")

Homes near rivers or the coast offer many amenities, but homebuyers need to consider and be prepared for the risks associated with buying a house in a flood zone. Real estate agents can connect home buyers with flood risk professionals who can help them make informed decisions about their desired location.

What Is a Flood Zone?

Downloadpdf (389 KB) | png (219 KB)

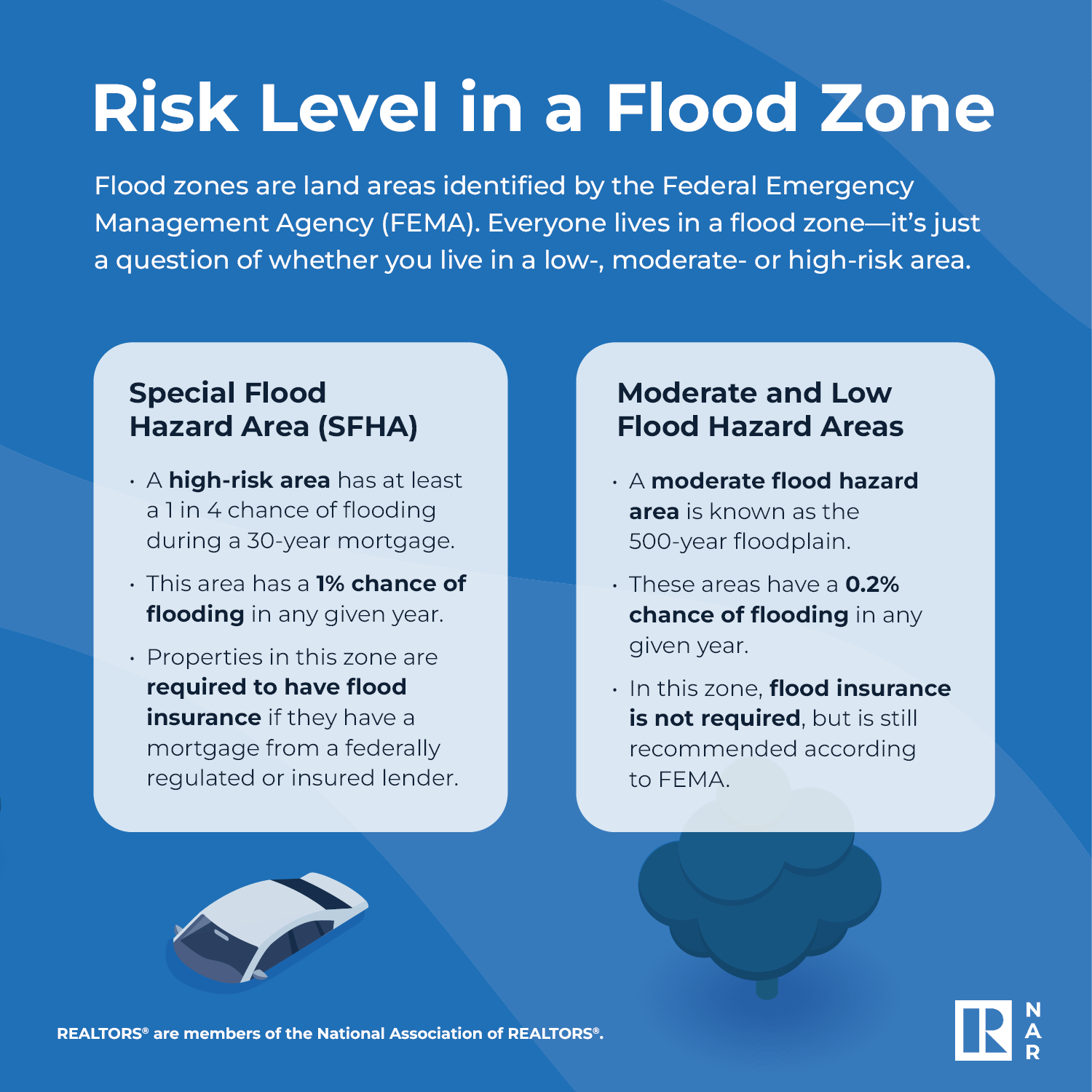

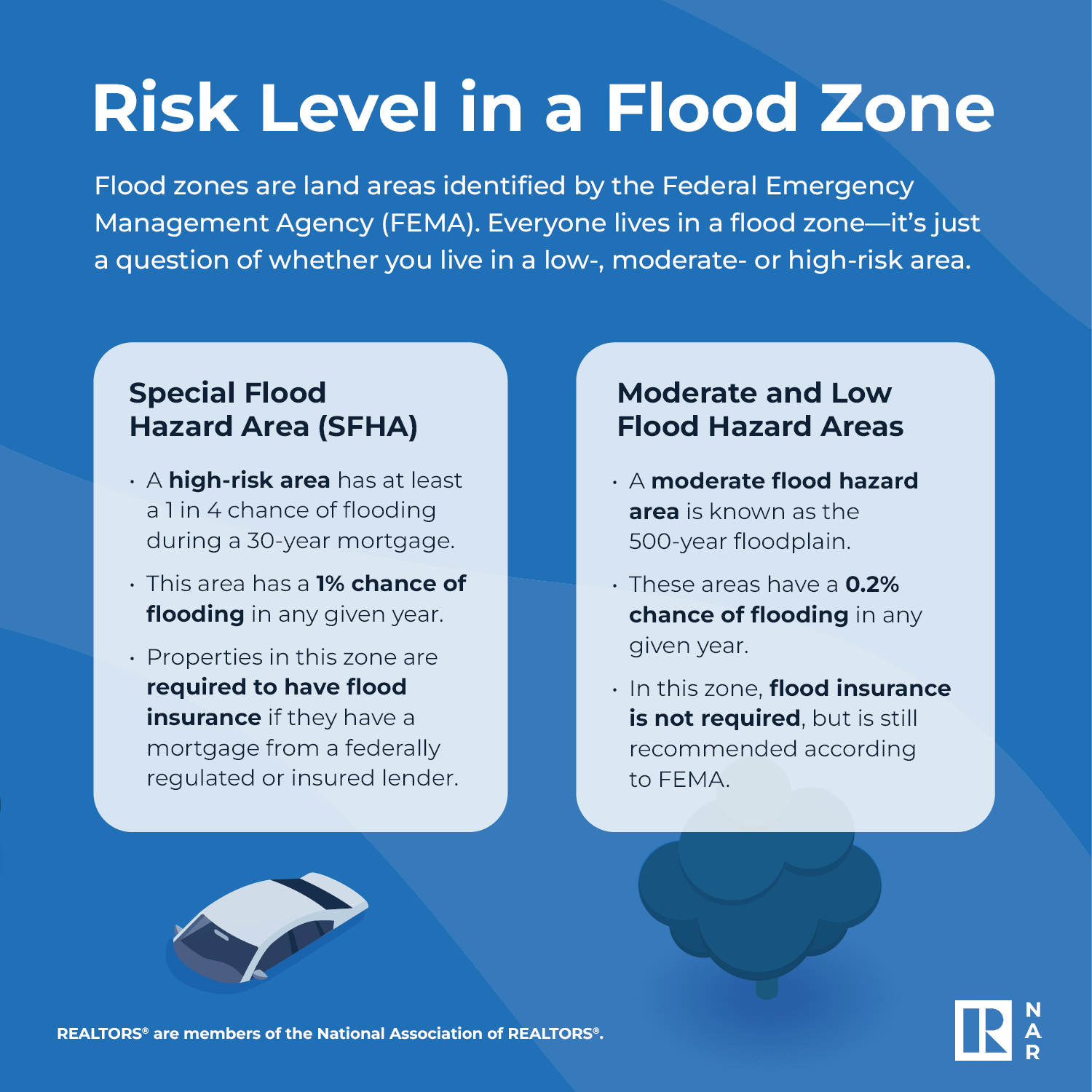

Special Flood Hazard Area (SFHA)

These are high-risk areas with a 1% chance of flooding in any given year and at least a 1 in 4 chance of flooding during a 30-year mortgage. Properties in this zone are required to have flood insurance if they have a mortgage from a federally regulated or insured lender. SFHAs are categorized as Zone A, Zone AO, Zone AH, Zones A1-A30, Zone AE, Zone A99, Zone AR, Zone AR/AE, Zone AR/AO, Zone AR/A1-A30, Zone AR/A, Zone V, Zone VE, and Zones V1-V30.

Moderate and Low Flood Hazard Areas

A moderate flood hazard area (Zone X, B, or C) is known as the 500-year floodplain; this area has a 0.2% chance of flooding in any given year. Flood insurance is not required in this zone, but is still recommended according to FEMA. Just because an area is designated “low to moderate” risk on an official FEMA flood map does not mean there is not significant risk.

Is My House in a Flood Zone?

The easiest way to find out if a client’s home or prospective home is in a flood zone is to use FEMA’s Flood Map Service Center. FEMA provides instructions on how to use the tool and read the map to help you get an accurate understanding of a home’s risk level.

Understanding which flood zone a house is in can play a critical role in buying decisions. Real estate professionals should be prepared to respond to client questions by providing contact information for a short list of flood risk professionals, including a state or local government floodplain manager (found through the Association of State Floodplain Managers), a licensed surveyor, and an insurance agent who offers flood insurance. Alternatively, your state’s EPA branch or your county's or city’s department of watershed management may offer additional resources and support for learning about flood zones in your region.

Flood Insurance

Flood insurance is federally required for a federally related mortgage in a special flood hazard area. While a lender may not require flood insurance in moderate- to low-risk zones on FEMA maps, FEMA has stated that there continues to be considerable risk everywhere and it’s advisable for buyers to consider purchasing flood insurance. As FEMA puts it, wherever it rains, it can flood.

Risks of Living in Flood Zones

Some of the risks that buyers seeking homes in flood zones may face include:

- Flood/water damage: Aside from severe floods with the potential to destroy property, according to FEMA just one inch of floodwater can result in damage to the tune of $25,000. For protection from flood damage, homeowners may need to pay high insurance premiums depending on the risk factors.

- Resale challenges: Houses in flood zones may be harder to sell later, even without weathering any actual floods. If the homeowners have suffered water damage and made flood insurance claims, it may be tough to find buyers willing to pay the asking price.

Tips for Real Estate Agents

If a client is considering purchasing a home in or near a high-risk flood zone, real estate agents should encourage clients to talk with a licensed insurance agent. Some insurance agents specialize in flood insurance. Real estate agents can help clients by having trusted flood insurance partners and experts available for referral.rance. Real estate agents can help clients by having trusted flood insurance partners and experts available for referral.

Review Disclosures

All 50 states require the disclosure of known material conditions or facts about property including prior flooding. States like Louisiana, Mississippi, New Jersey, New York and Texas have disclosure requirements beyond that. Real estate professionals should be familiar with their state’s disclosure laws and obligations under the REALTOR® Code of Ethics. NAR’s legal team has provided guidance on this.

Refer Clients to Insurance Agents

According to FEMA, the flood maps are not designed nor intended to be a reliable tool for home buyers to assess a property’s flood risk, and a property does not have to be near water to flood. For example, the maps do not reflect flood risks due to heavy rain, rising sea levels, melting snow, drainage system backups, and broken water mains, which helps explain why nearly one-third of flood insurance claims occur in the “low or moderate risk” areas. Instead of relying on the maps, FEMA recommends that home buyers make informed decisions by obtaining an NFIP rate quote through a licensed insurance agent or a new online Direct to Customer (D2C) Quoting Tool, which is now available on www.floodsmart.gov.

Look Beyond Flood Maps

Many credible organizations other than FEMA offer a more granular, current and accurate view of flood risk relative to the maps. For instance, see Climate Risks Reports for Every Property in the US | First Street. Real estate professionals may be the “source of the source” but they are not flood risk experts. Please do not discourage clients from considering credible sources and experts of flood risk information. The most important thing a real estate professional can do is to have ready the contact information for a short list of flood risk professionals.

Remember, wherever it rains, it can flood. An important fact that agents may provide is that from 2015 to 2019, 40% of flood claims came from outside high-risk areas. This means that while flood maps can give you a good starting point to understand flood risk, they don’t always tell you the whole story. Areas not designated “high risk” on a map aren’t necessarily immune to flooding.

{kind=link}