")

Increasingly unpredictable weather due to the ever-changing climate has led to more frequent flooding across the globe and the nation. Flooding in a home can wreak financial havoc on homeowners — just one inch of floodwater can result in over $25,000 in damage in a 2,500 square foot, one-story home. According to FEMA, wherever it can rain, it can flood. Having a flood insurance policy will help a property owner or buyer to pay for home repairs and replace personal belongings in the event of flooding.

What Is Flood Insurance?

Flood insurance covers losses directly caused by flooding that affects two or more acres of land or two or more properties. For example, damage caused by a sewer backup is covered if the backup is a direct result of flooding.

Standard property insurance policies do not include flood coverage, so property owners must be prepared to purchase a separate flood insurance policy either from the National Flood Insurance Program or a private insurance carrier.

Contrary to widespread belief, federal disaster aid is typically limited to a few thousand dollars and/or an SBA loan, which must be repaid with the mortgage loan; thus, flood insurance is more likely to help a property owner earn full compensation for damages.

Flood insurance is especially important since floods occur in 90% of all natural disasters in the U.S. Flood insurance is also required for homes with federally related mortgages in high-risk flood areas on Federal Emergency Management Agency maps and can provide peace of mind to homeowners as floods can occur anywhere, anytime.

The National Flood Insurance Program

The National Flood Insurance Program (NFIP) provides flood insurance to property owners to help them recover from flood damage. The program is managed by the FEMA and connects homeowners in 23,000 communities to a network of over 50 insurance companies. For more about the NFIP, please see NAR.realtor/flood-insurance.

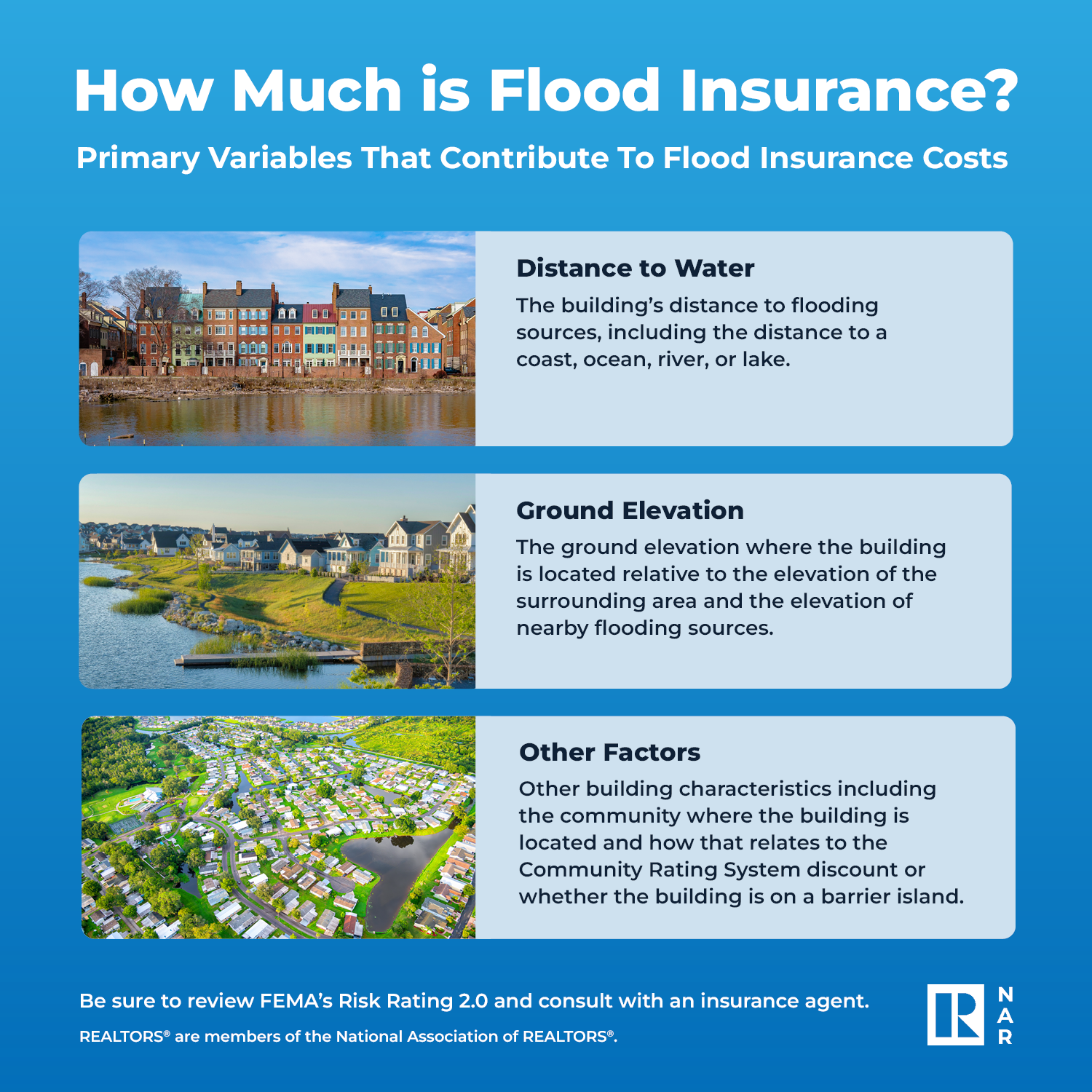

How Much Is Flood Insurance?

In setting prices, FEMA uses a rating methodology—Risk Rating 2.0: Equity in Action—which considers specific characteristics of a building to provide a more modern, individualized, and equitable flood insurance rate. Risk Rating 2.0 considers:

Downloadpdf (1 MB) | png (1 MB)

FEMA has provided a useful risk rating guidepdf. For more information, please consult an insurance agent.

Are Flood Insurance Rates Rising?

It depends. Under Risk Rating 2.0, NFIP insurance rates can rise or fall depending on changes in the building’s specific flood risk and replacement cost value. For rate quotes for individual properties, property owners and buyers should consult a licensed insurance agent. For estimates of recent nationwide rate changes, FEMA has prepared several analyses.

How to Lower Flood Insurance Costs

A licensed insurance agent can help a property owner or buyer to walk through NFIP’s coverage, deductible, and other options. Flood risk experts, including the local government floodplain manager, may be able to help identify home improvement projects, such as structure elevation or flood vents, to mitigate the flood risk to the property and therefore the property’s risk-based NFIP rate.

What Real Estate Agents Should Know About Flood Insurance

Most states require flood hazard disclosures by law, so check the State Flood Disclosure Tracker to be prepared. REALTORS®, members of the National Association of REALTORS®, should familiarize themselves with their duties under state law as well as NAR’s Code of Ethics. NAR’s Legal Affairs team has prepared a helpful guide.