Imagine this: You’ve found the perfect home for a buyer. They have secured financing and are preparing to close—only to discover that they can’t move forward without flood insurance. Lenders will require flood insurance before finalizing the loan if the property is in a Special Flood Hazard Area (SFHA). However, the standard homeowners insurance policy does not cover flooding. This means that without the National Flood Insurance Program (NFIP), the buyer would have to obtain flood insurance through the private market, which does not offer flood insurance in many areas across the United States. Property sales and loans could be delayed or halted nationwide in many flood zones if private flood insurance is unavailable. This disruption would not only affect buyers and sellers, but it could also create a ripple effect on the broader real estate market, related industries, and the economy.

In this analysis, we’ll explore how the NFIP supports and influences home sales and economic activity at both the national and local levels.

Impact on Home Buyers and Sellers

Without the National Flood Insurance Program, property owners and buyers must rely on the private insurance market, which does not provide flood insurance consistently. This presents a significant challenge for home buyers purchasing in FEMA-designated SFHAs because lenders require flood insurance as part of the mortgage approval process. As a result, many buyers in flood zones may face delays in closing their loans while waiting for flood insurance to be secured. Some contracts may expire if the delay lasts too long, causing buyers to renegotiate or withdraw from the sale. From a seller’s perspective, this results in longer listing times and added uncertainty in the market.

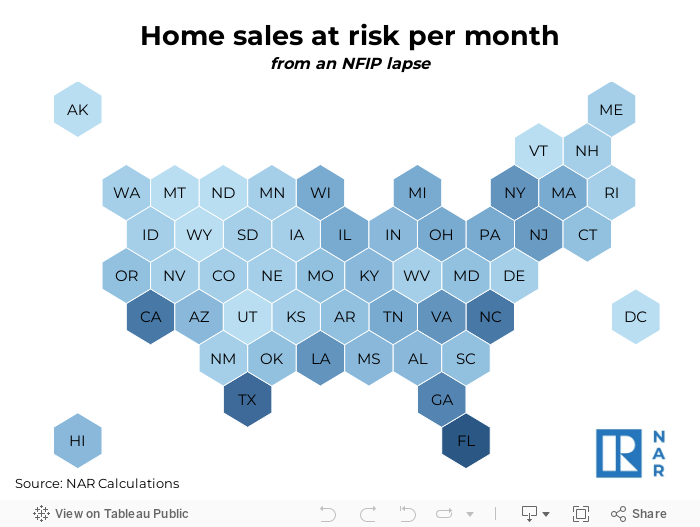

The National Association of REALTORS® (NAR) estimates that the NFIP is essential to 1,360 home sale closings daily, translating to approximately 41,300 affected monthly transactions nationwide.

While the impact varies by state, Florida’s housing market will be the most affected, followed by Texas and California. On a monthly basis, about 14,870 home sale closings in Florida depend on the NFIP. The program provides certainty for another 3,590 and 1,680 home sale closings in Texas and California, respectively.

Potential Economic Impact

Additionally, the housing market is a significant driver of economic activity. Beyond its primary function, the housing sector initiates a series of activities that propel economic growth, contributing to gross domestic product (GDP) through construction, home sales, and renovations. While these activities require labor and materials, they also stimulate production and job creation across multiple industries, such as construction, manufacturing, and retail. Furthermore, home purchases—particularly of older homes—typically trigger additional consumer expenditures. These new homeowners often invest in home improvement projects, furniture, appliances, and services to personalize and update their living spaces. However, the economic impact of the housing sector extends even further. The construction of new homes and renovating existing ones requires labor, which creates a wide range of jobs, from architects and builders to interior designers. Moreover, the real estate sector employs many professionals, including agents, brokers, and mortgage lenders. Thus, the ripple effects of a booming housing market can substantially reduce unemployment and boost people’s incomes.

After estimating the income generated by every home sale for each state, NAR estimated that without the NFIP, total income losses could reach $69.7 billion per year. This figure is approximately equal to Alaska’s GDP.

The map below shows the breakdown of the economic benefit of the NFIP by state. Without NFIP, Florida ($23.0 billion), California ($5.5 billion), and Texas ($4.9 billion) lead the list with the largest local income losses per year.

Given the scale of these economic effects, ensuring stable and reliable access to flood insurance is crucial—not just for those buying and selling homes, but also for maintaining broader market and economic stability.