Overall, the office market continues to see negative net absorption, rising vacancy rates, and lower asking rent in 2021 Q3 compared to one year ago. This is due to the ongoing weak demand for office space in the primary or gateway markets, with about half of computer/tech workers still working from home nationally. However, secondary markets are experiencing an increase in office occupancy, given the relatively affordable residential and commercial prices in these markets, according to NAR's September 2021 Commercial Monthly Insights Report.

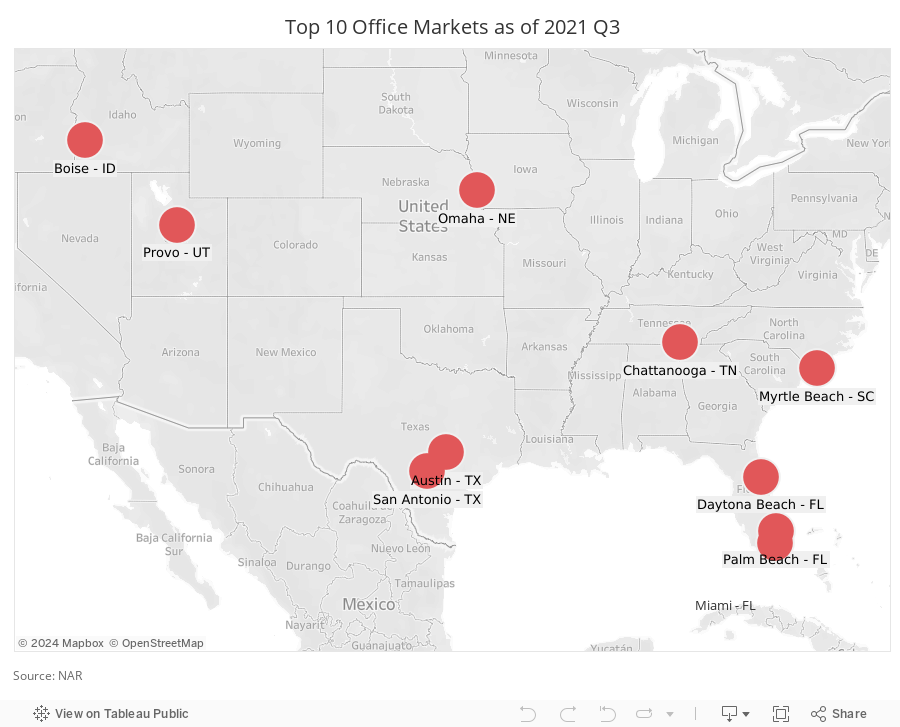

NAR identified ten markets with the strongest office market conditions as of 2021 Q3. In alphabetical order, the markets are:

- Austin, Texas

- Boise, Idaho

- Chattanooga, Tennessee

- Daytona Beach, Florida

- Miami, Florida

- Myrtle Beach, South Carolina

- Omaha, Nebraska

- Palm Beach, Florida

- Provo, Utah

- San Antonio, Texas

NAR identified these markets by comparing 10 commercial and economic indicators in these markets to the national level figures: vacancy rates, 12-month net absorption, year-over-year change in asking rent growth, leasing volume in square feet, year-over-year percent change in business/professional jobs of the metro area, net delivered units over a 12-month period, sales transactions in dollars, transaction sales price per square feet, and cap rate.

A point was given for every metric where the market had stronger market conditions (e.g., the vacancy rate is lower than nationally). These markets had an aggregate score of at least 50 (equal to, or outperformed, the US market). In addition, only markets that had positive net absorption over a 12-month period as of September and with a population of at least 500,000 in 2020 were included.

Austin, Texas

Austin had the highest leasing activity, at 1.9 million square feet. It had the second-largest net absorption in the past 12 months of 924,626, second to Palm Beach. Austin had the highest average sales transaction price at $584/square feet, with an average return on investment (cap rate) of 5.4% compared to 7% nationally, which indicates the premium put on Austin commercial office space. The office vacancy rate of 13.5% is slightly higher than the national rate of 12.4%, but this won't remain elevated for long due to the strong absorption of office space in Austin.

Boise, Idaho

Boise has one of the lowest vacancy rates, at 4.7% compared to 12.4% nationally. The average office asking rent was up 1.6% compared to a decline of 0.4% nationally. Boise absorbed 895,328 square feet of office space, the third-highest among the top 10. Office space in Boise is relatively cheaper, with an average sales transaction price of $140/square feet, and a cap rate of 6.3%.

Chattanooga, Tennessee

Chattanooga has a low office vacancy rate of 4.3% so the average asking rent was up 2.3% year-over-year as of September 2019, the third-highest rent growth after Palm Beach and Daytona Beach. With a cap rate of 6.7%, properties are still relatively cheaper compared to Austin or Miami.

Daytona Beach, Florida

Daytona had a vacancy rate of just 5%, with year-over-year rent growth of 2.9%. The average sales transaction price in the third quarter was $128/square feet with a cap rate of 6.6%, about the same as Chattanooga and Provo. Daytona Beach prices are more affordable compared to Miami and Palm Beach, which are also in the top ten list. Daytona Beach is likely to attract more workers with the opportunity to work from home and retirees who enjoy time at the beach and Florida's warm weather.

Miami, Florida

Miami is second to Austin in terms of leasing activity, at 1.2 million square feet. Its vacancy rate is relatively high compared to the other markets, at 10.7%, but this is still a tad lower than the national vacancy rate of 12.4%. Office properties are more expensive, with the average sales price at $383/square feet, but investors are willing to pay the price for Miami property and get a 5.7% return on their investment that is lower than the national rate of 7%.

Myrtle Beach, South Carolina

Myrtle Beach has the lowest office vacancy rate among markets in this list, at 2.2%. With a tight vacancy rate, it has the second-highest average asking rent growth of 2.9%. Myrtle Beach is also a favorite vacation spot, and its county, Horry County, is one of the top 30 largest vacation home counties. Myrtle Beach is likely to see more migration into the area from workers who have greater opportunities to work from home and from retirees who envision beach destinations.

Omaha, Nebraska

Among the markets in the top 10, Omaha had the lowest average price sales price in the third quarter, at $122/square feet, and the highest cap rate of 8.3%. Omaha has a somewhat high vacancy rate of 8.9%, but this is still lower than the national rate of 12.4%. Office rents are up just 0.4% compared to the faster pace of rent increases in the Florida metros.

Palm Beach, Florida

Palm Beach beats all markets in terms of the 12-month net absorption of office space of 1 million square feet and with net absorption of about 853,000 of office square feet. Palm Beach's vacancy rate is also relatively high at 9.9%, but this is lower than Miami's rate and nationally. The price of office space is a bit more affordable than in Miami, with the average sales transaction price of $318/square feet compared to $383/square feet in Miami.

Provo, Utah

Provo absorbed 793,154 square feet of office space in the past 12 months with 852,792 of office space leased. Commercial office space is one of the cheapest, at $177/square feet. The average cap rate was 6.7% compared to Boise's 6.3%. The vacancy rate in Provo is also somewhat high compared to Austin, at 9.3%, more than double that of Boise, although its vacancy rate is below the national rate.

San Antonio, Texas

San Antonio is benefiting from the strong growth in the Austin market given its proximity to Austin and its more affordable residential and commercial prices. It has a lower vacancy rate than Austin, at 10.1%. As such, the area is experiencing faster office rent growth of 1.7% compared to Austin's 0.5%. The average transaction price of office sales in the third quarter was $145/square feet, about a fifth of Austin's, yielding a cap rate of 6.3%, which is about a percentage point higher than Austin's.