On a national level, office vacancy rates continued to rise in the first quarter of 2021 to 16.4%, from 13% one year ago. But the impact of the pandemic has varied across areas, with the gateway and tech-heavy cities seeing huge spikes in vacancies arising from subleases while smaller secondary/tertiary markets have seen relatively minor increases in vacancy rates, according to NAR's latest Commercial Market Trends and Outlook Report.

Primary Cities See Huge Increases in Office Vacancy Rates, but Modest Rise in Secondary/Tertiary Cities

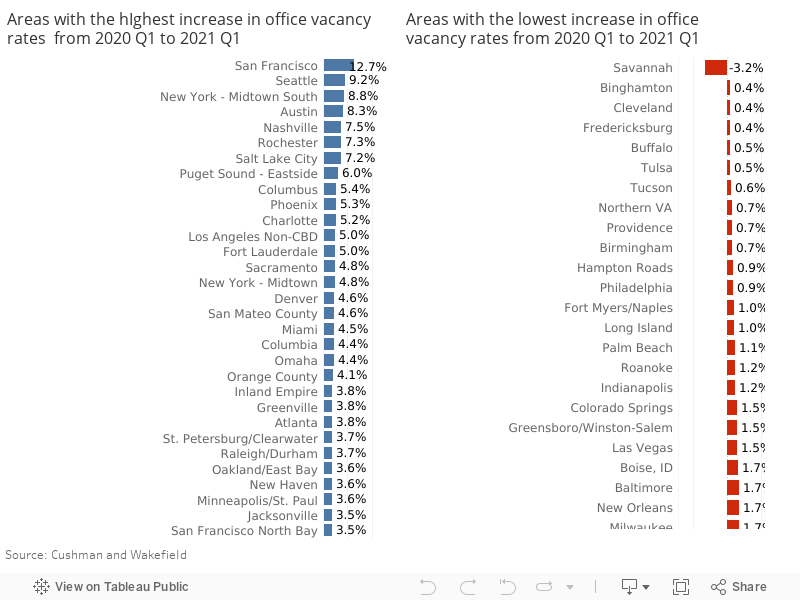

In San Francisco, the overall vacancy rate (direct and available via sublet) has increased by a whopping 12.7 percentage points as of 2021 Q1 from one year ago (6% to 18.7%), as 9.7 million square feet of office space became unoccupied, according to market data from Cushman and Wakefield. In Seattle, the overall vacancy rate increased by 9.2 percentage points (8% to 17.2%), as 4.3 million square feet of office space became unoccupied. The New York-Midtown South shed the most office space, at 10.7 million square feet, which led to an 8.8 percentage points increase in vacancy rate ( 8.2% to 17%). Cities with a relatively large tech workforce such as Austin, Nashville, Rochester, Salt Lake City, and Puget Sound (which includes Seattle) also saw a surge in overall vacancy rates.

On the other hand, vacancy rates have only increased modestly in most secondary or tertiary cities. One reason could be attributed to the Paycheck Protection Program that helped small businesses stay in business and enabled the small business owners to keep paying rent and to work out arrangements with landlords. With the pandemic affecting the entire economy, landlords would also have found it difficult to get new office tenants. According to the U.S. Census Business Pulse Survey, less than 2% of small businesses have closed permanently, even if half are operating at below normal capacity.

There are also location-specific factors accounting for the modest increase in vacancy rates. In Savannah, the office vacancy rate even declined, with office leasing activity benefiting from Savannah's strong industrial commercial real estate market because of its growing port operations and pickup in distribution and warehousing, with an industrial vacancy rate at a low 3.4%. Fort Myers/Naples is benefiting from the expansion of medical offices in the area. In Tucson, the Foothills submarket also had continuing lease-ups. Tucson is benefiting from relatively low office rents compared to Phoenix.

Gateway Cities Suffer Huge Declines in Occupancy While Areas That Had Higher Occupancy Were Secondary/Tertiary Markets

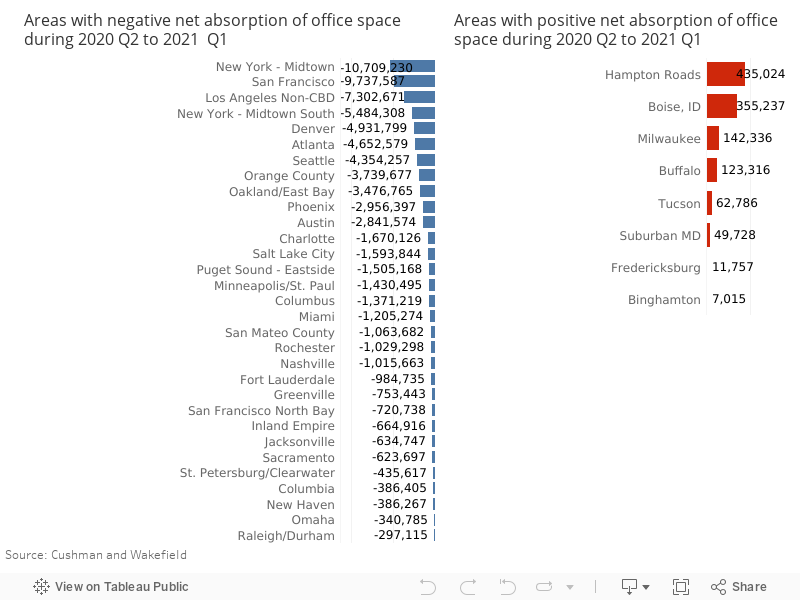

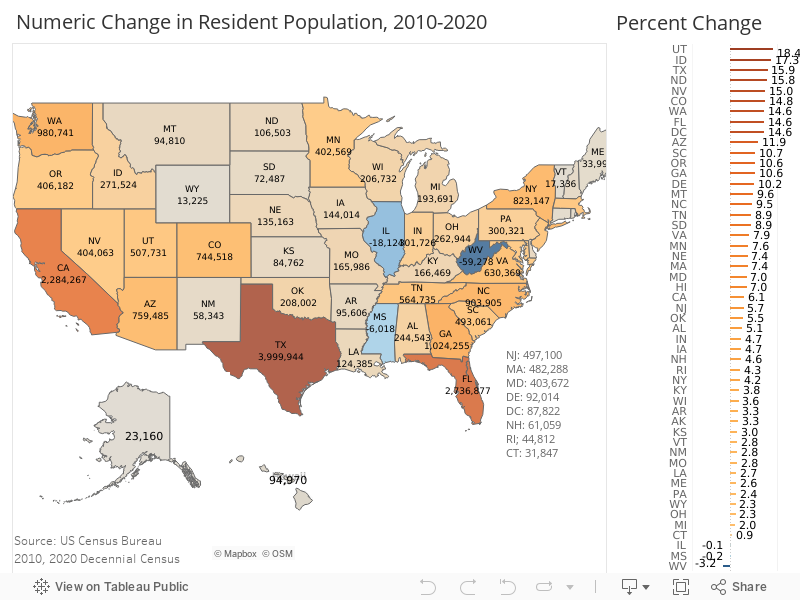

Only the secondary/tertiary markets saw an increase in office occupancy in 2021 Q1 compared to one year ago. These are Hampton Roads, Boise, Milwaukee, Buffalo, Tucson, Suburban Maryland, Fredericksburg, and Binghamton. The demand for office space in Hampton Roads is likely associated with the strong growth in the industrial/logistics development in Hampton Roads (Brookwood Development's Portside Logistics, Commerce Park in the Harbor View, Coastal Logistics Center).1 Boise is not surprising given that Idaho was the state with the highest percentage increase in population during 2010 to 2020 based on the 2020 decennial survey that was recently released. As noted earlier, Fort Myers/Naples is benefiting from the expansion of medical offices in the area. In Tucson, the Foothills submarket also had continuing lease-ups, with Tucson benefiting from relatively low office rents compared to Phoenix. In Milwaukee, little corporate downsizing has taken place.2

Vacancy Rates Rising Due to Subleases

Nationally, the office vacancy rate continued to tick up in the first quarter of 2021, to 16.4%, from 13% one year ago. Vacancy rates continue to increase, with 21% of the workforce still working from home as of March 2021 (6% prior to the pandemic), and even higher at 58% among computer and mathematical workers.3 Vacancy rates have increased as occupiers shed 138.4 million square feet of office space.4

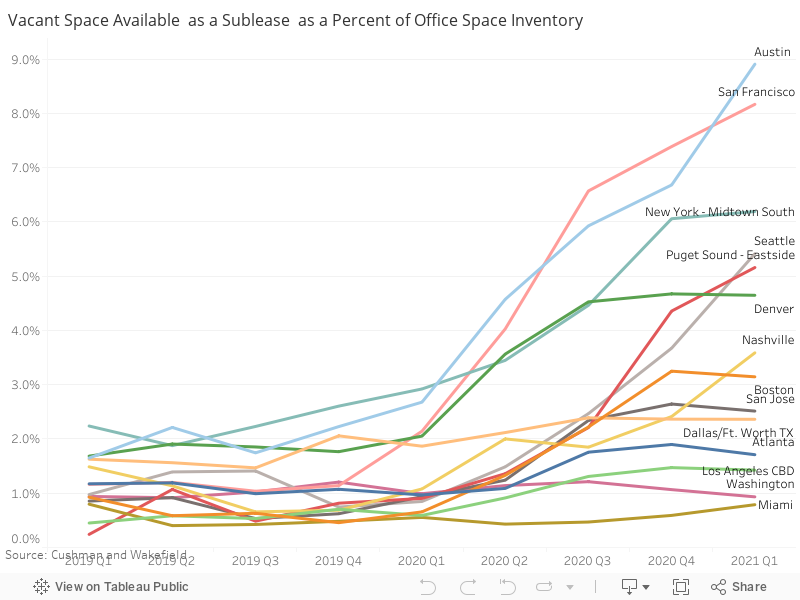

Vacancies available through sublease are a large part of the overall vacancy rate in big cities with heavy tech and financial industry base. Direct tenants are still leasing the office space, but with workers working at home, the unused office space is being sublet. The available office space from flexible operators like WeWork is also part of this subleased vacancy, and tech workers and startup companies have been the largest occupiers of flexible office space.

Austin, San Francisco, New York-Midtown, Seattle, Puget Sound are areas that have seen a large increase in vacant space that is offered via subleases. In Austin and San Francisco, the vacancy that is available through sublet rose to 8% of office space from just 2% a year ago.

Secondary/Tertiary Areas Office Market See Huge Increase in Asking Rents

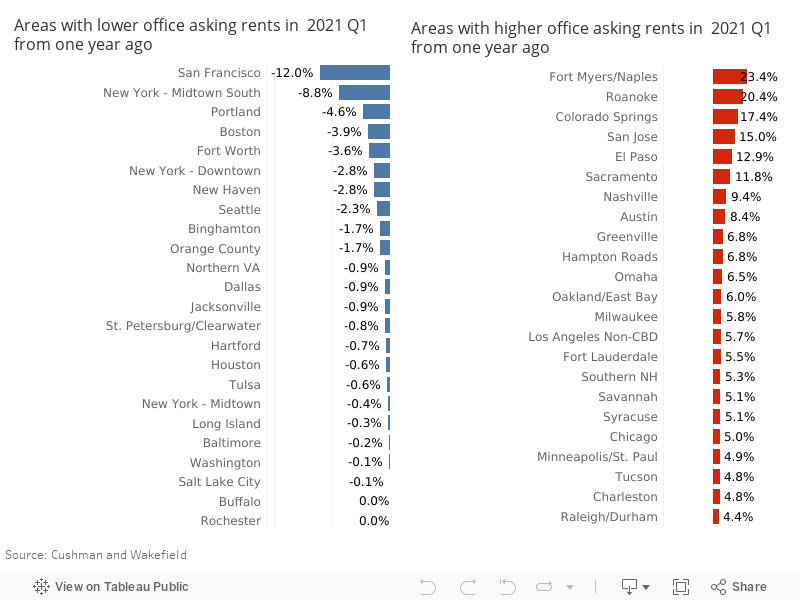

In the areas with high vacancy rates, asking rents have dropped tremendously as of 2021 Q1 from one year ago, such as in San Francisco (-12%) and New York Midtown South (-9%). But in cities with low office vacancy rates, asking rents have sharply increased by as much as over 15%, such as In Fort Myers/Naples (+23%), Roanoke (+20%), and Colorado Springs (+17%).

Surprisingly, asking rents continued to increase even in San Jose (15%), Nashville (9%), and Austin (8%) even as vacancies have increased sharply in these areas. Nationally, asking rents were up 5% year-over-year as of 2021 Q1, according to Cushman and Wakefield market data. However, while asking rents have not declined, most landlords have been providing tenant concessions. This is because the pandemic is a temporary shock to the office market, so landlords are not lowering asking rents for leases that extend beyond the pandemic's short-term impact. Instead, they are granting concessions to lower the current rents. Fifty-five percent of NAR commercial members who responded to the latest quarterly commercial survey reported that they are seeing more tenant concessions compared to the pre-pandemic period.

Cities in States With Strong Population Growth Likely to See Sustained Demand for Office Space

The secondary markets that are found in states with growing population such as Idaho (Boise), Utah (Salt lake), Texas (Dallas, Austin, Houston, San Antonio), Florida (Fort Myers), and Virginia (Hampton Roads) will likely continue to see a demand for office space. Nationally, the recovery of the demand for office space in the big cities hinges on workers returning to their offices. As earlier noted, much of the vacancy is being driven by subleases, with slightly more than half of computer/mathematical workers still working from home. Not all will likely return to the office, and assuming that 5% of the additional employment that is generated is work from home, vacancy rates will likely continue to increase to about 18% in 2022.

1Cushman and Wakefield, https://www.cushmanwakefield.com/en/united-states/insights/us-marketbeats/hampton-roads-marketbeats

2 https://www.cushmanwakefield.com/en/united-states/insights/us-marketbeats/milwaukee-marketbeats

3 Source: American Community Survey in 2019 and BLS COVID-19 supplemental survey

4How big is 138.4 million square feet? A football field is around 57,600 square feet, so the negative net absorption is equivalent to 2,403 football fields, or 48 football fields per state.