One major impact of the coronavirus pandemic is on where people are deciding to live, work, and play. The desire to live in less dense areas given the uncertainty of the course of the coronavirus pandemic as new variants emerge, the ability of people to work from home and reduce travel time and costs, and the demographic boost to housing in the suburban areas as millennials continue to form households and raise families are all factors that play into the decision of where people will be living and buying a home.

ln this blog, I look at housing market indicators in the outlying and central counties of metropolitan or micropolitan areas to assess homebuyer preference to live in the central counties or live farther out of the metropolitan centers. As of June 2021, housing market indicators show outlying counties of metropolitan or micropolitan areas are experiencing more robust housing demand compared to the central counties, indicating that housing demand is dispersing outwards from the central counties of metropolitan or micropolitan areas to outlying counties.

Methodology and data source (realtor.com®)

For this analysis, I used realtor.com® home listings summary statistics in 1,000 counties, of which 883 are central counties and 114 counties are outlying counties of a metropolitan or micropolitan area based on the U.S. Census Bureau March 2020 delineation.1 According to the U.S. Census Bureau, " a central county is a county or counties of a Core Based Statistical Area (metropolitan statistical area or micropolitan statistical area) containing a substantial portion of an urbanized area or urban cluster or both, and to and from which commuting is measured to determine qualification of outlying counties. An outlying county is a county that qualifies for inclusion in a core based statistical area on the basis of commuting ties with the CBSA's central county or counties."2

Housing indicators in central and outlying counties

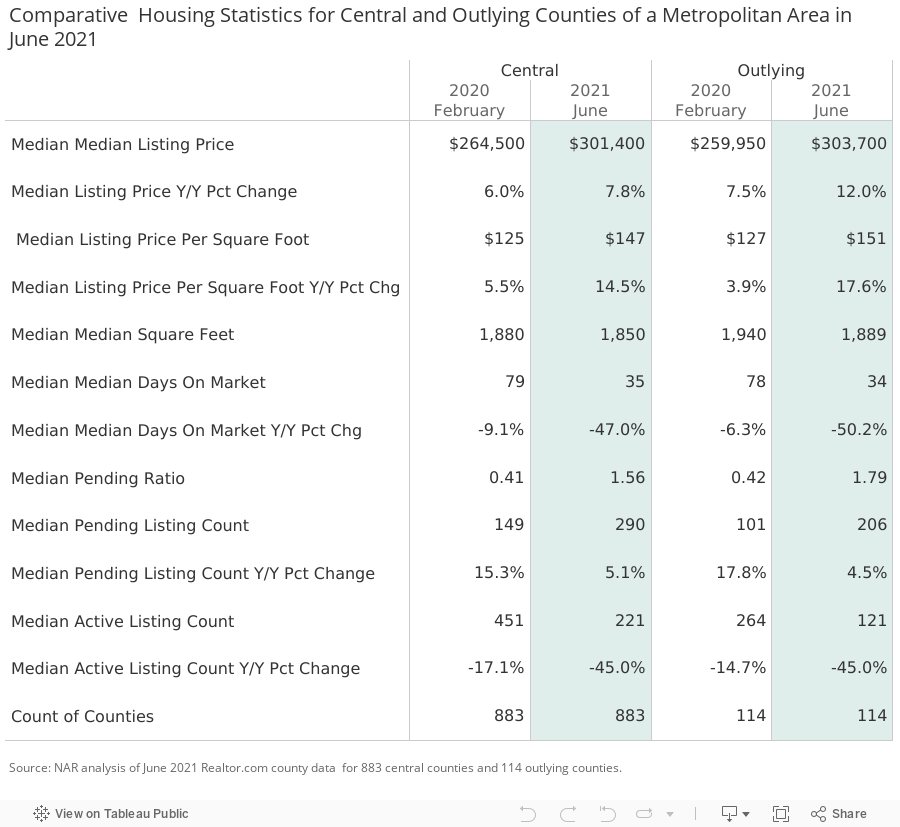

Home listings data from realtor.com® as of June 2021 indicates that housing demand in outlying counties of metropolitan areas is growing at a more robust pace than in the central counties, although both outlying and central counties are performing remarkably well compared to pre-pandemic conditions (February 2020).

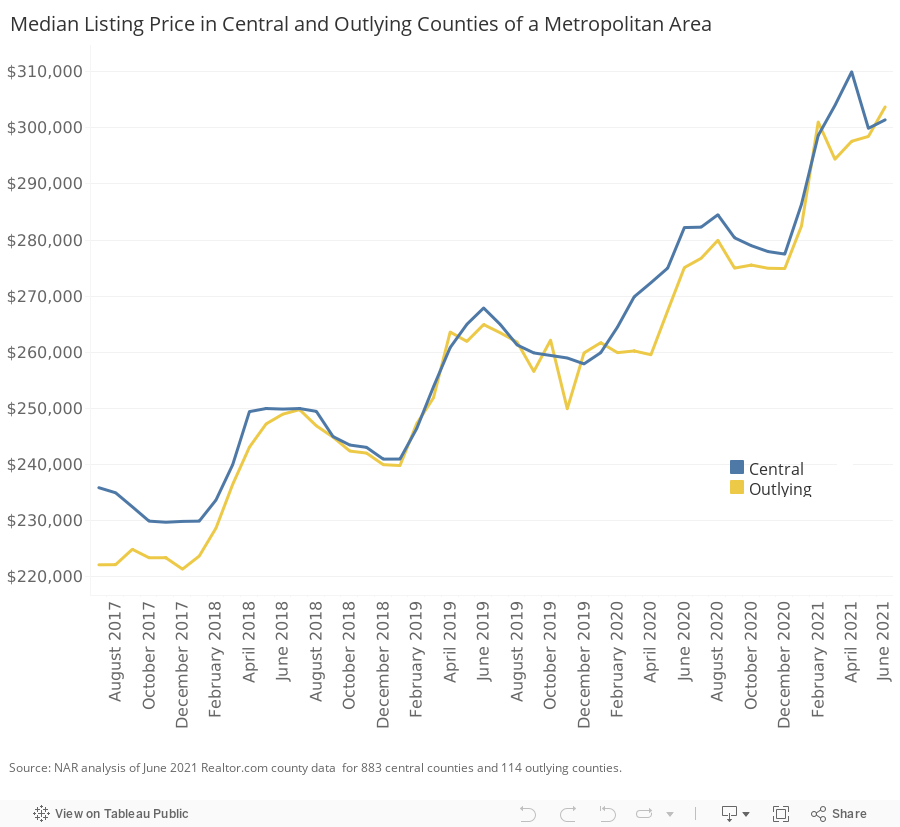

Faster price appreciation in outlying counties. In June, the median listing price in outlying counties rose 12% from one year ago, while the median listing price in central counties rose at a slower pace of 7.8%. The median price appreciation of listing prices has decelerated in the central counties while the pace of price appreciation in outlying counties rebounded in June after a slight deceleration in May to 9.8%.

In fact, the median listing price in the outlying counties was slightly higher at $303,700 compared to the median listing price of $301,400 in central counties. The median listing price per square foot is also higher in the outlying counties, at $151/square feet compared to $147/square feet in the central counties.

Fewer days on market in outlying counties. Properties in both central and outlying counties are selling at about half the pace compared to one year ago, but properties are selling a day faster in outlying counties, at 34 days, compared to 35 days in the central counties. One year ago, the median days on market in outlying counties was 78 days, a day faster than in the central counties.

Active listings are down in both central and outlying counties while pending listings are up. The typical number of homes that are actively listed on any given day in a month are down 45% in both central and outlying counties, indicating a severe lack of supply in both areas.

On the other hand, pending listings are up in both central and outlying counties, with a slightly higher rate of increase of 5.1% in central counties compared to outlying counties, at 4.5%.

Higher ratio of pending listings per active listings in outlying counties

Bringing together both demand (pending listings) and supply conditions (active listings), there is a higher imbalance between demand and supply in outlying counties, with a median of 1.8 pending listings per active listing compared to 1.6 pending listings per active listing in the central counties.

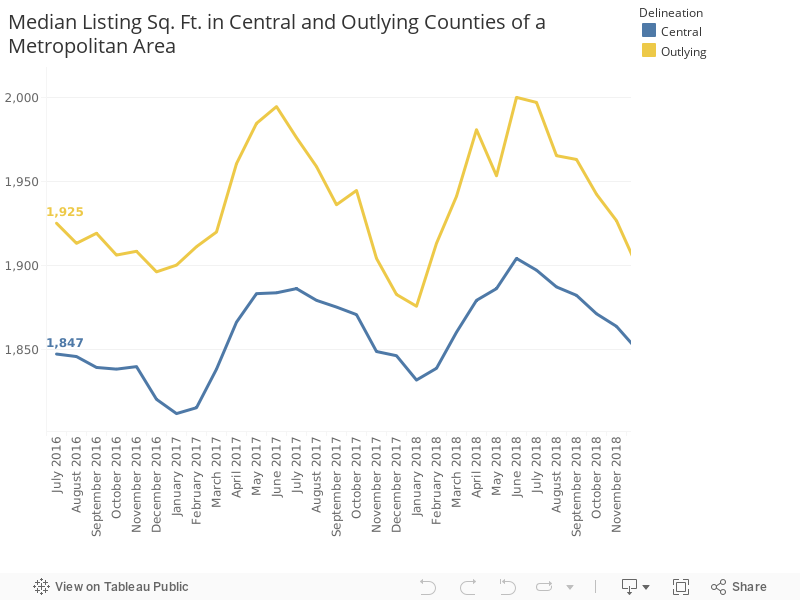

Bigger square footage in outlying counties

One reason for the preference of a home in the outlying counties is the availability of bigger homes and more yard space. In terms of the home square footage, the median square footage of homes listed in outlying counties was 1,889 square feet which is 39 square feet larger than the median square footage of 1,850 square feet in the central counties. That 39 square feet gives extra storage space or even a little corner area that can be used as a work area.

Median listing prices in selected metro areas

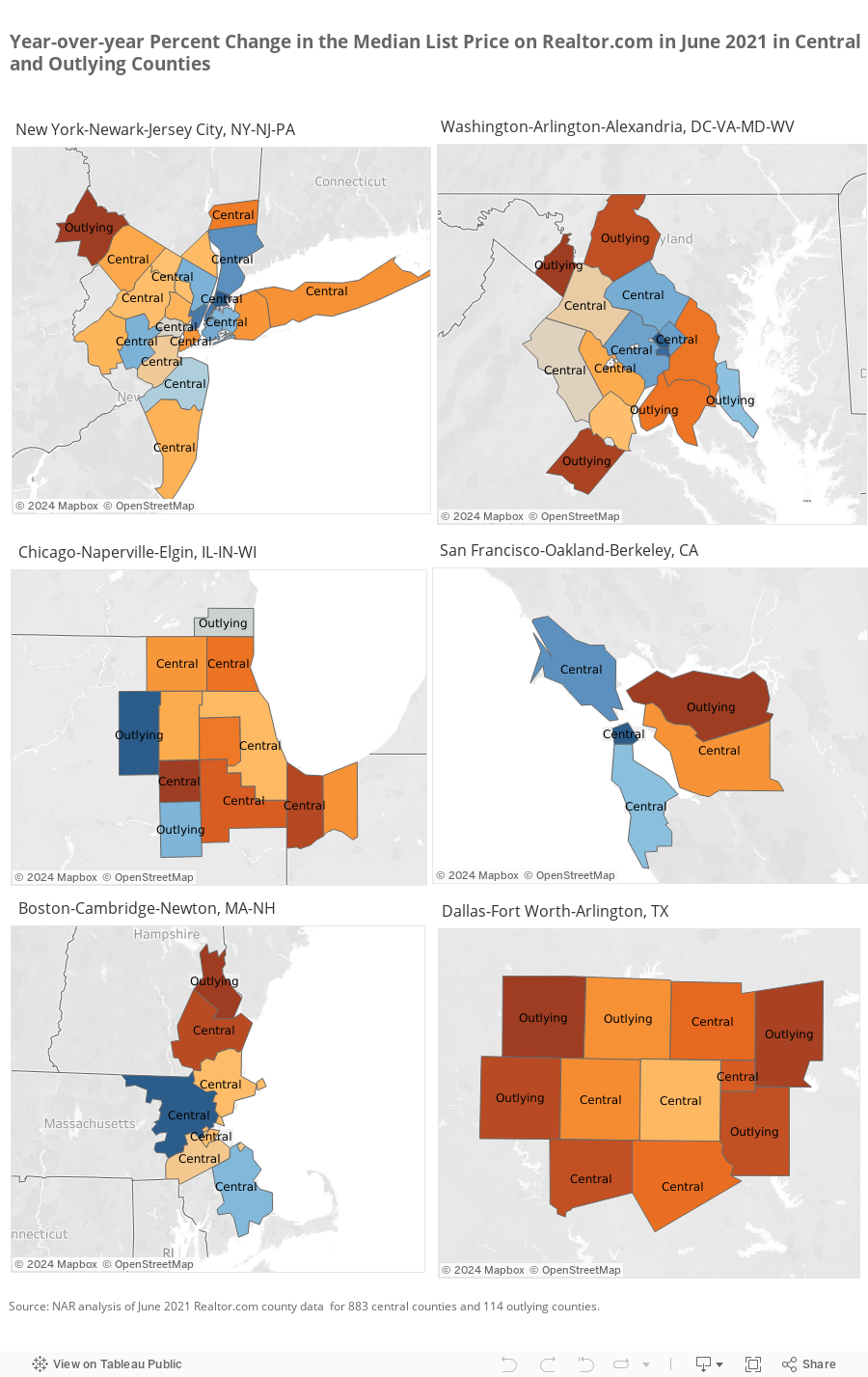

Drilling down into the major metro areas for which there is at least one outlying or central county tracked by realtor.com®, median listing prices are rising at a faster pace in the outlying counties compared to the central counties.

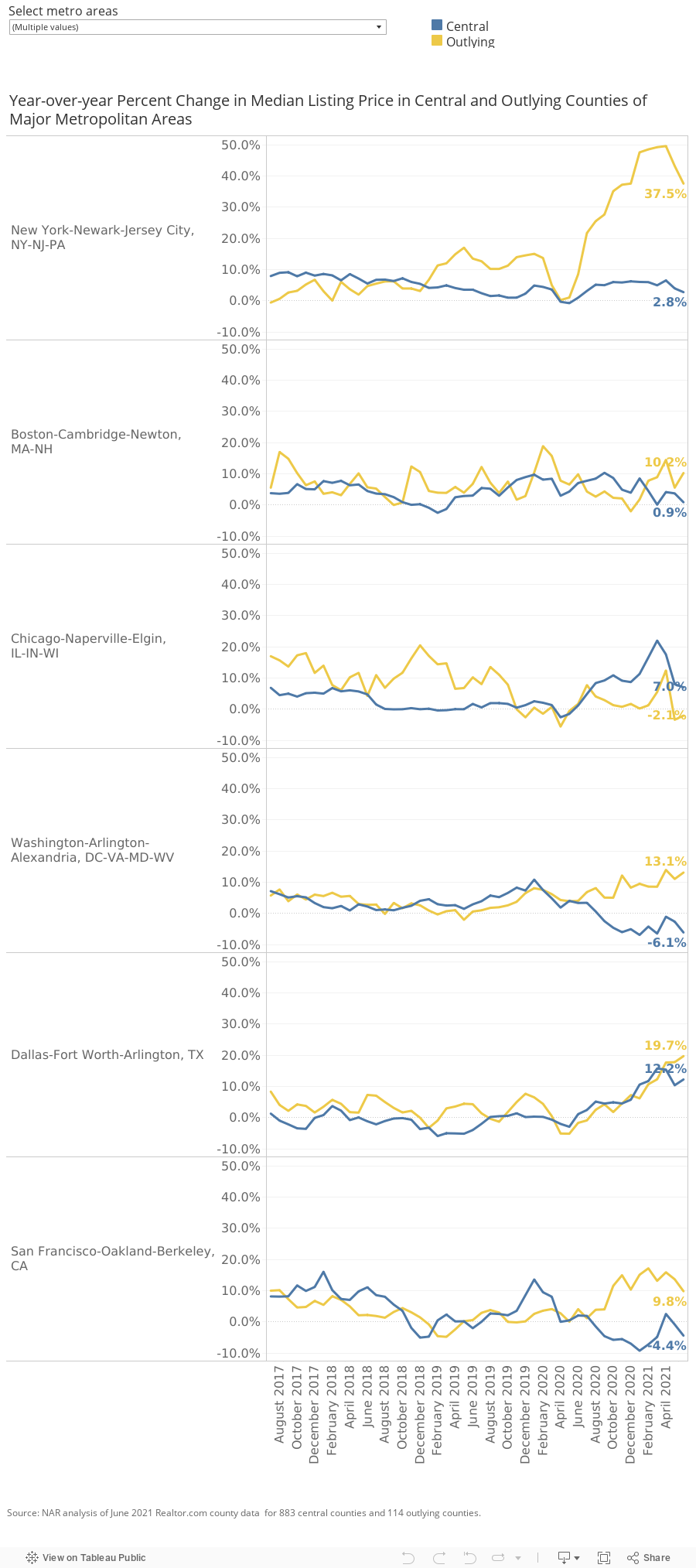

For example, in the New York-Newark-Jersey City area, the median price in the central counties is just up by 2.8% year-over-year in June 2021 due to price declines in central counties like Kings (-4.6%), Queens (-3.3%), Bronx (-12.8%), Westchester (-7%), and Bergen (-3.9%). However, prices are rising in the central counties that are vacation spots like Suffolk (12.3%) and Nassau (11.5%) and Ocean, New Jersey (6.3%). The only outlying county for this metro area that is tracked by realtor.com® is Pike, Pennsylvania where the median list price rose 37.5% year-over-year.

In the Washington-Arlington-Alexandria metro area, list prices in June 2021 were down in the District of Columbia (-15.4%) and the central counties of Fairfax (-15%), and Montgomery (-12.3%). However, list prices were up in the outlying counties of Spotsylvania, Virginia (15.4%), Jefferson, West Virginia (16.6%), and Frederick, Maryland (13%). However, the median list price declined in the outlying county of Calvert, Maryland (-7.1%).

The Chicago-Naperville-Elgin metro area is bucking the trend where home prices are falling in the outlying counties such as DeKalb (-7.3%) while listing prices are rising in the central counties such as Cook (2.1%). The city of Chicago is in Cook County.

In the San Francisco-Oakland-Berkeley metro area, the median list price is down in the central counties of San Francisco (-11.6%), Marin (-6.4%), and San Mateo (-2.4%). However, Alameda, a central county, is showing price appreciation (3.2%) as well as the outlying county of Contra Costa (9.8%). San Francisco is a county that has been taking a long time to recover because its workforce is heavily concentrated in technology jobs. Nationally, 50% of computer/mathematical workers are teleworking as of June 2021 compared to 14% among all occupations.

In the Boston-Cambridge-Newton metro area, the median list price is down year-over-year in the central county of Middlesex (-3.3%) while other central counties of Norfolk (0.6%), Suffolk (1.1%), and Essex (1.2%) are showing modest price growths. In the outlying county of Strafford, New Hampshire, the median list price is up double digits (10.2%). The city of Boston is in Suffolk. This indicates that cities are not dead, although housing demand is growing more robustly in the outlying counties.

In the Dallas-Fort Worth-Arlington metro area, the median list price in the central county of Dallas is growing at a modest pace (3.2%) compared to the nearby central county of Tarrant (8.3%) or the outlying counties of Hunt (22%), Wise (23.5%), and Ellis (11.8%).

Homes in outlying counties are less expensive and offer more space

Affordability is clearly a driver of the demand for homes in outlying areas. Homes in outlying counties have been generally less expensive than in central counties. However, in June 2021, the median list price in outlying counties notched up slightly above the median list price in central counties, indicating the strong demand for housing in outlying counties.

Homes are also larger in outlying counties. In June 2021, the median listing square feet of homes listed in outlying counties rose to 1,889 square feet. On the other hand, the median listing square feet in central counties has been falling since 2020, from 1,951 square feet to 1,850 square feet as of June 2021. This indicates that homeowners are selling smaller homes and that the homes that are left on the market as actively listed are the smaller homes, indicating a preference for bigger homes.

Homes with work-from-home spaces remain desirable to homebuyers, according to NAR's latest June REALTORS® Confidence Index survey. In this monthly survey, 58% of REALTORS® reported that they had a buyer who was looking for features that can be used as space to work from home, such as a finished basement, an extra room, nook, or den.

Housing Demand Outlook in Outlying Counties

Demand in central counties that are home to big cities has been weaker, but as of now the data does not show a collapse in home prices in the cities (e.g., Boston, Chicago, Dallas). San Francisco and New York are the cities facing the toughest recovery in terms of the demand for housing (owned and rented) and office space, but housing demand is holding up in secondary or tertiary cities.

However, if the trend towards working from home is sustained, and if jobs start moving towards outlying counties, the strong demand for both larger homes and less expensive homes in the outlying counties will likely continue and will outpace demand in the central counties of metropolitan areas.

Of course, other factors will affect the demand for housing in outlying counties, such as the presence of good schools (for millennial households) and efficient transit or road commutes (for those who will be on a hybrid schedule) from residences to places of work, school, and leisure. The bipartisan infrastructure bill which is intended to repair and rebuild the network of roads and bridges to improve the efficiency, equity, and safety of commuters will be instrumental in connecting the outlying counties to the central counties and principal cities of metropolitan areas.

1 I categorized the realtor.com® 1,000 metro areas as central or outlying counties based on the March 2020 U.S. Office of Management and Budget Bulletin delineation; https://www.census.gov/geographies/reference-files/time-series/demo/metro-micro/delineation-files.html. The three counties that realtor.com® tracks that are not in the March 2020 OMB Bulletin and could not therefore be classified into central or outlying counties are Van Buren, Michigan; Barry, Michigan; and Le Flore, Oklahoma.

A central county is a county or counties of a Core Based Statistical Area containing a substantial portion of an urbanized area or urban cluster or both, and to and from which commuting is measured to determine qualification of outlying counties. An outlying county is a county that qualifies for inclusion in a Core Based Statistical Area on the basis of commuting ties with the Core Based Statistical Area's central county or counties. A county qualifies as outlying under the following circumstances: (1) one-quarter or more of the employed residents work in the central counties of the metropolitan or micropolitan statistical area, or (2) one-quarter or more of the employment is composed of workers who live in the central counties. Furthermore, outlying counties also include the counties of any smaller metropolitan or micropolitan statistical area that are adjacent to the metropolitan or micropolitan statistical area and merge with it. https://www.census.gov/programs-surveys/metro-micro/about/glossary.html

2 To note, outlying counties are not the same as "suburbs" which are popularly considered as places that border the cities or towns and have strong economic relationships (people live there but work in the city). For example, in the case of the Washington-Arlington-Alexandria metro area, both Fairfax County and the District of Columbia are considered central counties although the popular notion is to consider Fairfax County as a suburb of Washington, DC.