Homeownership among women in the U.S. has been on the rise over the past two decades. Between 2005 and 2023, the national female homeownership rate1 increased from 61.1% to 63.0%, approaching the male rate (67.7% in 2023). The increasing trend is reflected in the recently published Profile of Home Buyers and Sellers 2024 report, which revealed that 20% of home buyers that year were single women, the largest share of buyers after married couples. For a closer look at data on single women in the Profile of Home Buyers and Sellers, read this blog post. To add to the understanding of the successes and challenges faced by female homeowners in the current market, we analyze data at the local level, focusing on metropolitan areas and marital status.

In 2023, women owned more homes than men in 31 of the country’s major metropolitan areas. The typical2 female homeowner was younger (57 years vs. 58 years), had less income ($76,695 vs. $90,088), and owned less expensive property ($264,037 vs. $283,440) compared to male homeowners. Yet, female homeowners earned a higher income than male homeowners in 19 metro areas and owned more expensive property in 59 areas that year.

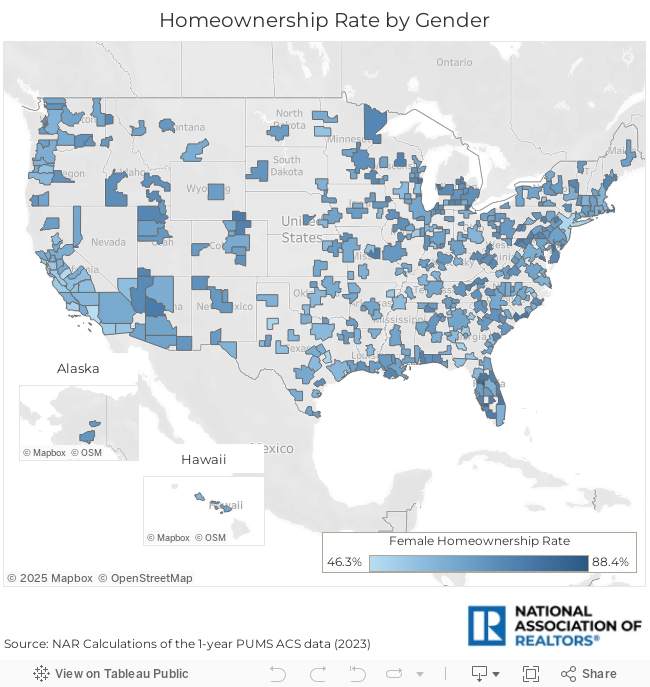

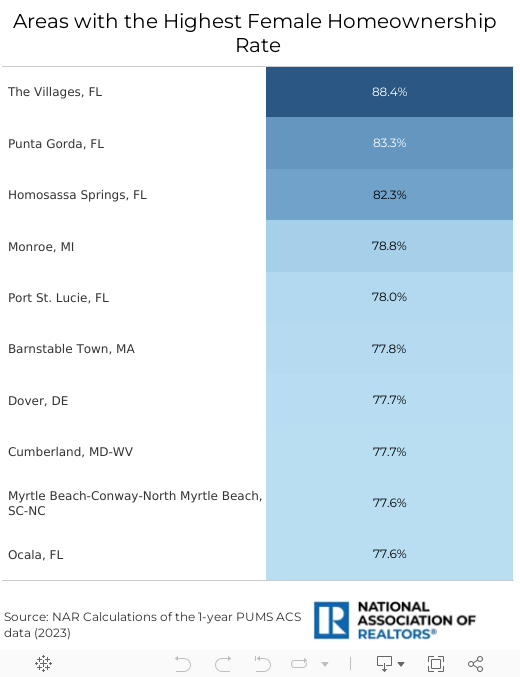

The highest female homeownership rate was in The Villages, FL (88.4%). It was followed by Punta Gorda, FL (83.3%), Homosassa Springs, FL (82.3%), and Monroe, MI (78.8%). Notably, five of the top 10 areas with the highest female homeownership rates were in Florida. In contrast, the area with the lowest female rate was Los Angeles-Long Beach-Anaheim, CA, where only 46.3% of women owned homes. It was followed by Merced, CA (48.1%), New York-Newark-Jersey City, NY-NJ-PA (48.7%), and Lawrence, KS (48.8%).

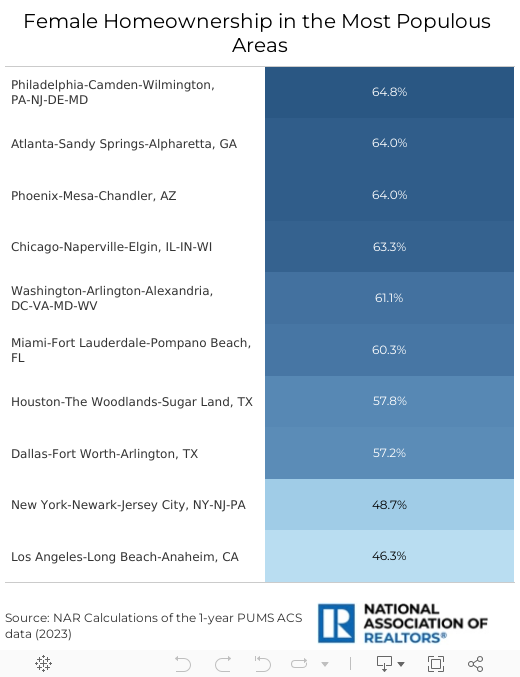

Among the most populous metropolitan areas, the share of women who owned homes was the highest in Philadelphia-Camden-Wilmington, PA-NJ-DE-MD (64.8%). It was followed by Atlanta-Sandy Springs-Alpharetta, GA (64.0%), Phoenix-Mesa-Chandler, AZ (64.0%), and Chicago-Naperville-Elgin, IL-IN-WI (63.3%).

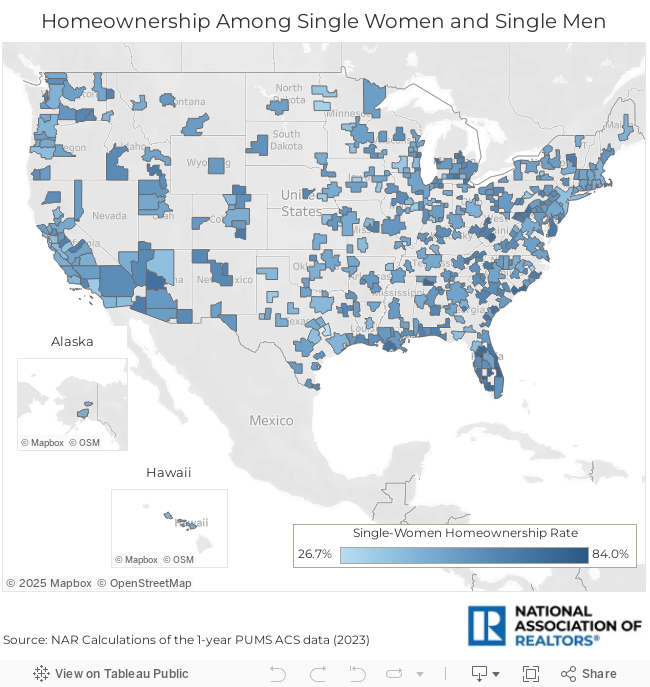

In recent years, single women3 have also been experiencing a significant rise in homeownership rates; however, they were older and owned less expensive homes than married women. In 2023, the typical single woman homeowner was 68 years old, with an income of $41,240, and a property valued at $221,174—while the typical single male homeowner was younger (60 years old), had a higher income ($54,523), and owned a slightly more expensive property (valued at $226,054). Despite that, single women owned more homes than single men in 295 metro areas and owned more expensive properties than men in 185 areas.

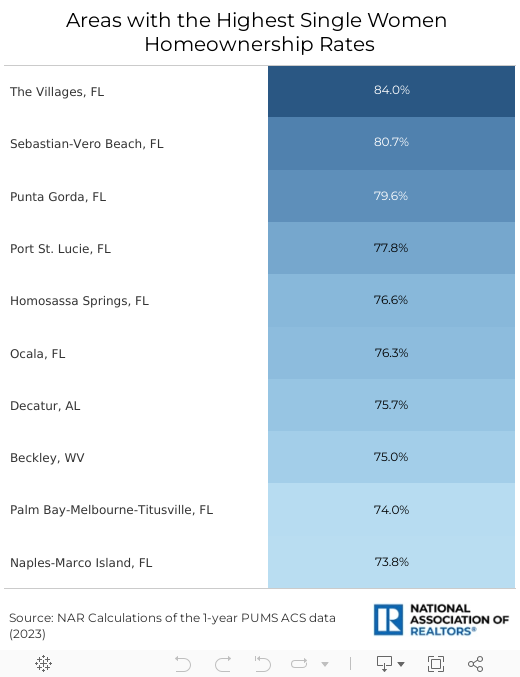

The Villages, FL (84.0%) had the highest homeownership rate among single women, as well as the highest overall female homeownership rate. In fact, eight of the top 10 areas with the highest homeownership rate for single women were in Florida. The Villages area was followed by Sebastian-Vero Beach, FL (80.7%), Punta Gorda, FL (79.6%), and Port St. Lucie, FL (77.8%).

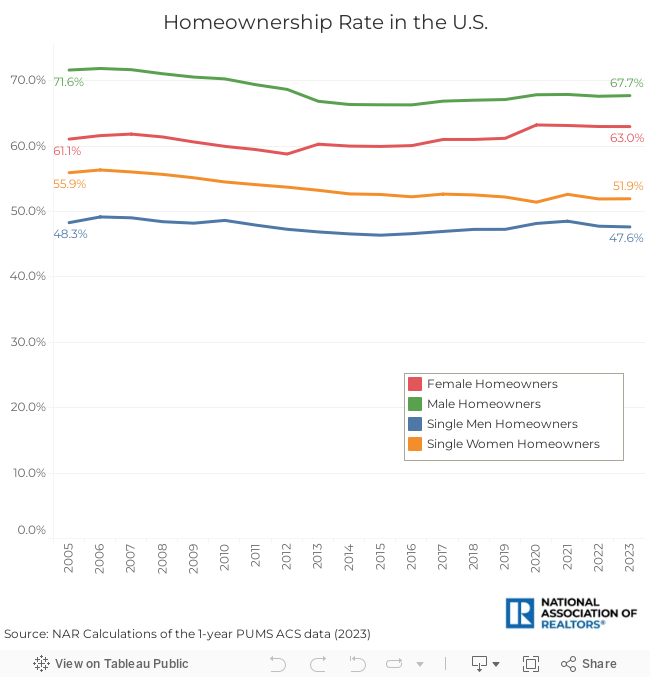

Historically, men had the highest homeownership rates, with a peak of 71.9% in 2006, just a couple of years before the onset of the Great Recession. However, male homeownership has declined since then; homeownership among men declined by 3.9 percentage points, from 71.6% in 2005 to 67.7% in 2023. In contrast, the female homeownership rate has been steadily growing, increasing by 1.9 percentage points from 61.1% in 2005 to 63.0% in 2023. The homeownership rate among women reached its highest point in 20204 at 63.2%, compared to 67.8% for men in the same year. Additionally, the difference between female and male homeownership rates has been narrowing over the last two decades. In 2005, the difference was 10.5 percentage points, but by 2023, it had decreased to 4.7 points.

For single households, both single men and single women experienced a slight decrease in homeownership rates in the last 18 years. Nevertheless, following the national trend, the difference between single women's and single men's homeownership rates narrowed from 7.6 percentage points in 2005 to only 4.3 points in 2023. The gap is closing, and non-married owners, especially single women, are making notable progress.

1 Homeownership rate is calculated as the number of male or female homeowners divided by the number of male or female households.

2 Refers to the median female or male homeowner with median age, median annual income, and median property value owned.

3 Single, when used as a marital status category, is the sum of never married, widowed, and divorced people aged 18 and above.

4 Due to the COVID-19 pandemic, there may have been data quality issues in the data collected in 2020.

Anat Nusinovich

Anat Nusinovich is an Economist for the National Association of REALTORS®.

Advertisement