With strong U.S. industrial fundamentals as of December 1, 2021, the record shattering continues. The industrial sector is on pace for a historical year despite the supply chain issues that had an impact on the shipping of goods. Considering consumer spending trends, elevated digital sales and increasing retail spending will continue to put pressure on crucial supply chain hubs, e.g. seaports, especially with the holiday season underway. Demand for U.S. industrial space completed Q3 2021 with record-setting statistics: with demand outpacing supply for the fourth consecutive quarter as a lack of available supply aided in pushing rents upwards as well as record low vacancy rates.

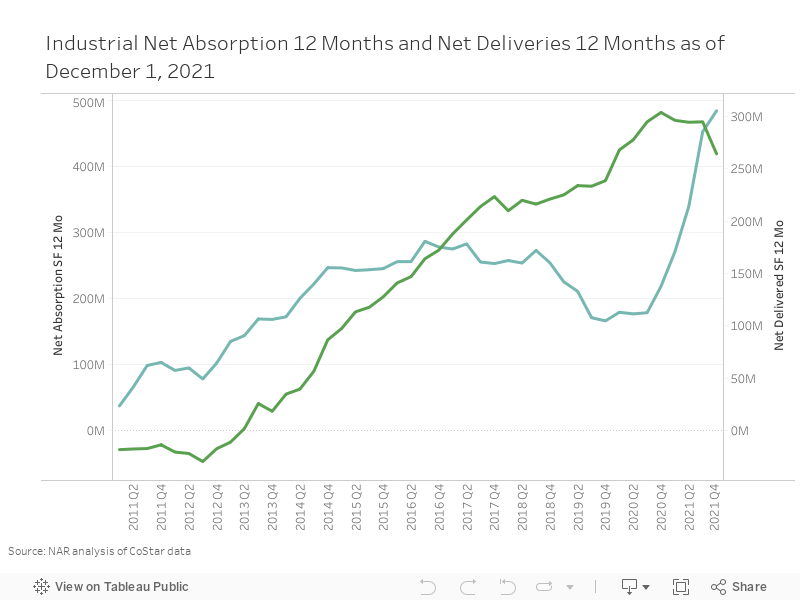

While all industrial fundamentals have notched new records across the board and remained quite strong thus far in Q4 2021, net absorption was the most striking. As tenants occupied industrial space, as of December 1, 2021 and two months into Q4 2021, 12-month net absorption already exceeds the 453 million square feet (msf) recorded in Q3 with a total of 485 msf, as all-time highs continue to be set. The increased demand and limited availability of industrial space continues to put pressure on industrial’s already historically low vacancy rate, which saw another decrease as it hit a new low of 4.2%. With declining vacancy, rents for industrial space were in $9.51 in Q3 and increased to $9.72 as of December 1, 2021. Year-over-year rents have increased by 8.2%. According to CoStar® data covering 390 metros, all 390 metros had positive year-over-year rent growth where markets such as Miami, FL (14.0%), Northern New Jersey, NJ (13.7%), Nashville, TN (13.0%), Philadelphia, PA (12.8%), and Fort Lauderdale, FL (12.3%) were the top markets with highest rent growth.

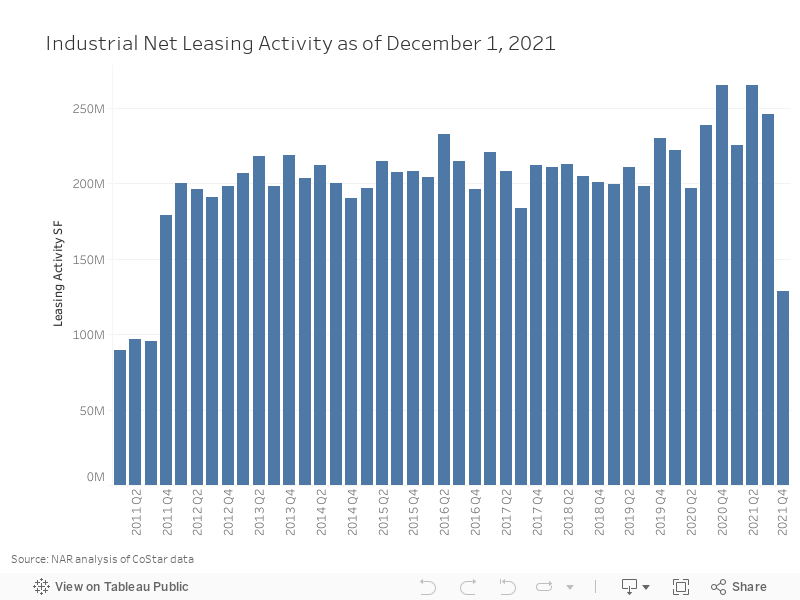

New leasing activity surpassed 200 msf for the fifth consecutive quarter in Q3 2021 at 246 msf. As of December 1, 2021, this brought the year-to-date (YTD) total to 865 msf. This level of demand in new leasing activity is on pace to surpass last year’s historical 923 msf by year-end and is driven by demand for logistic space.

Although industrial demand is quite potent, the limited availability and lack of supply illustrate a skewed relationship. Net delivery of industrial space totaled 78 msf in Q3 while 12-month net delivery totaled 295 msf. As of December 1, 2021, net delivery is at 48 msf while 12-month net delivery sits at 264 msf, both of which are below demand which introduces more competition amongst tenants for industrial space. Phoenix, AZ, Memphis, TN, Dallas-Fort Worth, TX metros were leaders with an increase in net deliveries in their metro as of Q4 2021, while 12-month net deliveries were led by Dallas-Fort Worth, TX, Inland Empire, CA, and Houston, TX. Q3 saw the highest amount of industrial space under construction at 466 msf. Although net deliveries are increasing, the lack of space could continue should the difference between supply and demand widen.

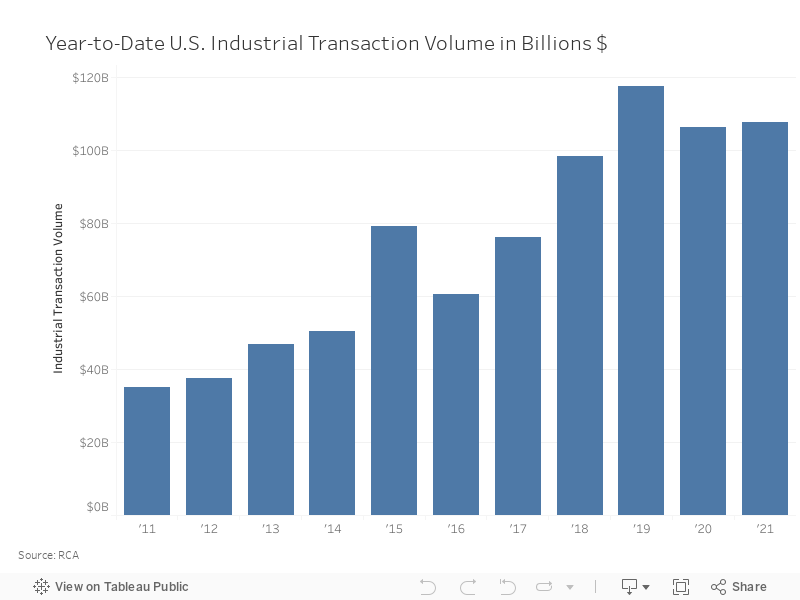

However, industrial space remains a top priority amongst investors as a result of strong asset fundamentals where industrial transaction volume totaled $9.9 billion in October 2021, a 17% year-over-year volume increase. YTD industrial sales volume totals $107.6 billion and represents a 48% year-over-year increase, as demand for industrial properties are as stout as ever.