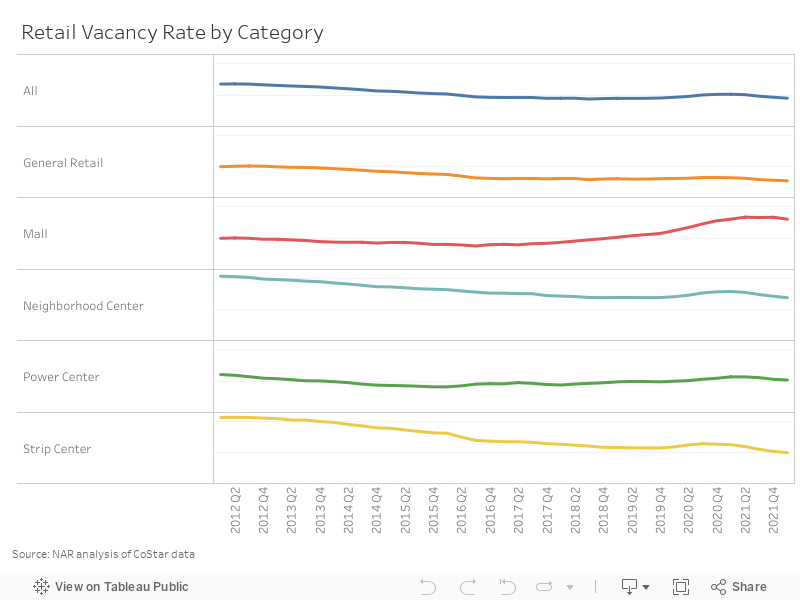

The retail vacancy rate declined throughout 2021 and ended Q4 2021 at 4.7%, down from the previous quarter's 4.8%. Retail vacancy as of Q1 2022 is down to 4.5%.

The lowest vacancy is reserved for general retail (2.7%) while power center and strip center vacancy were relatively close to one another at 5.2% and 5.0%, respectively. Mall and neighborhood center vacancy, while declining, remain slightly elevated at 8.0% and 6.9%.

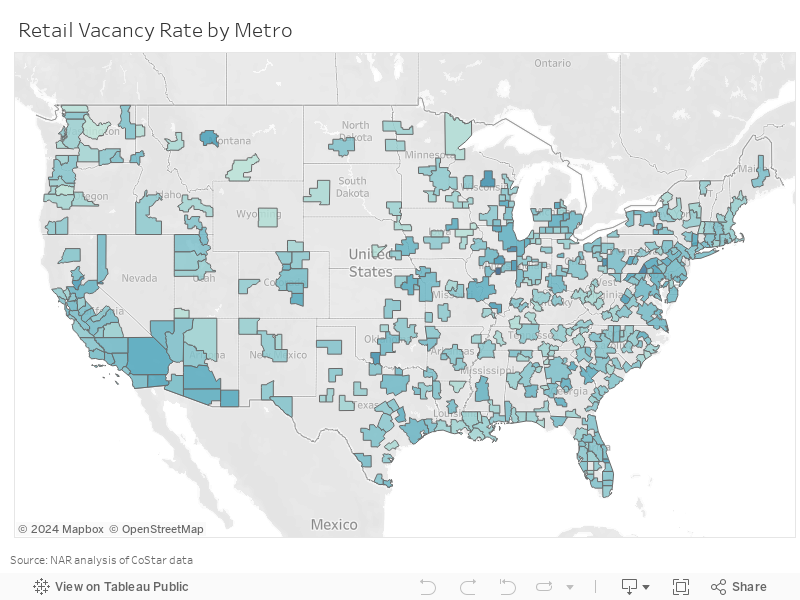

The highest retail vacancy rates were in the Decatur, IL and Chambersburg-Waynesboro, PA markets at 12.8% and 10.7%, respectively, while the lowest retail vacancy rates were seen in western states: Wenatchee, WA (0.6%); Billings, MT (0.9%); Albany, OR (0.9%); Dubuque, IA (1.0%); Bellingham, WA (1.0%); Cedar Rapids, IA (1.1%); St. George, UT (1.1%); Coeur d'Alene, ID (1.2%); and Casper, WY (1.3%). The lowest retail property vacancy rates by the six major retail metro markets1 were as follows: Seattle (2.6%), New York (4.0%), Atlanta (4.3%), Dallas (5.0%), Los Angeles (5.2%) and Chicago (5.9%).

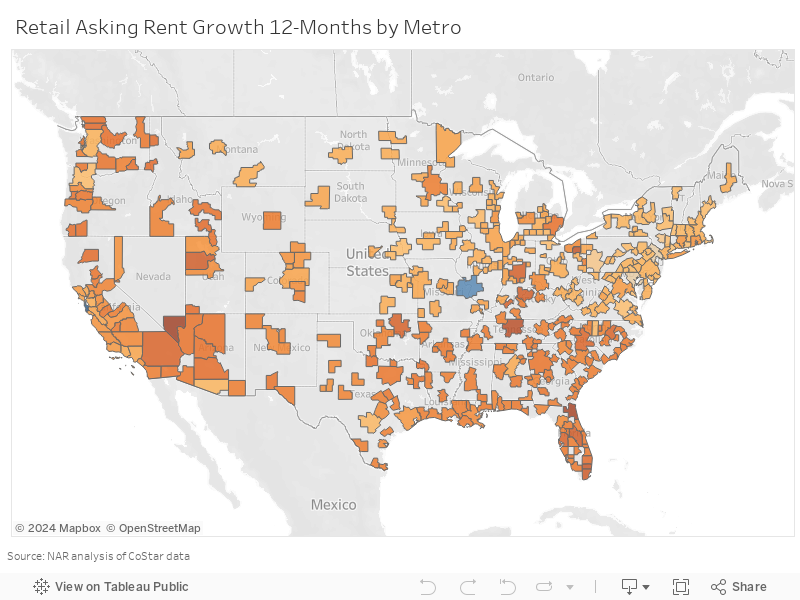

The continuous decline in retail vacancies puts upward pressure on asking rents, upwards to $22.63 for 3.2% annual growth from Q4 2020 to Q4 2021. As of March 17, 2022, rents rose to $22.90 for 3.9% annual growth. Positive retail asking rent growth is occurring in 99% of 390 metro areas, according to NAR's analysis of asking rent data.2 Leaders in asking rent growth both exhibit double-digit rates and are occurring in Las Vegas, NV (11.4%) and Jacksonville, FL (11.0%). The majority of positive rent growth inside the top 10 are located in the Sunbelt and in Florida in particular where Florida metros make up 40%.

Florida's retail market is quite hot. Furthermore, backing up to the top 20 markets with positive rent growth over the past 12 months reveals that Florida metros make up a third with several metros experiencing rent growth of at least 6.5% such as Jacksonville (11.0%), Fort Lauderdale (8.6%), Miami (8.1%), Orlando (8.0%), Tampa (7.4%) and Palm Beach (6.7%).

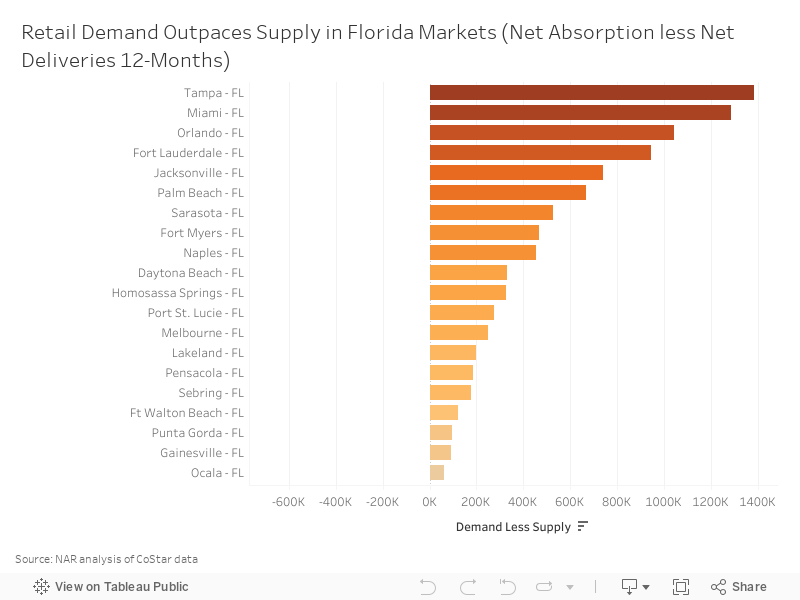

As of March 17, 2022, and of the 24 Florida markets analyzed, 87% of Florida metros saw retail demand (net absorption 12-month) exceed that of supply (net deliveries 12-month). Thus, Florida's asking rent growth should continue an increasing trend. In Tampa, there was more than 1.3 million square feet that was absorbed by the market in comparison to the square footage that was delivered in the past 12 months, followed by Miami (1.2 million square feet) and Orlando, at 1.0 million square feet.

1 Based on historical sales deal size, the six major retail commercial metro areas prior to the pandemic were Los Angeles, New York, Chicago, Dallas, Seattle, and Atlanta.

2 According to CoStar® market data