Elevated demand for industrial space continues as consumer spending habits trending toward the convenience of online shopping persist. Given the current state of e-commerce and last-mile demand, industrial remains the market with the strongest fundamentals.

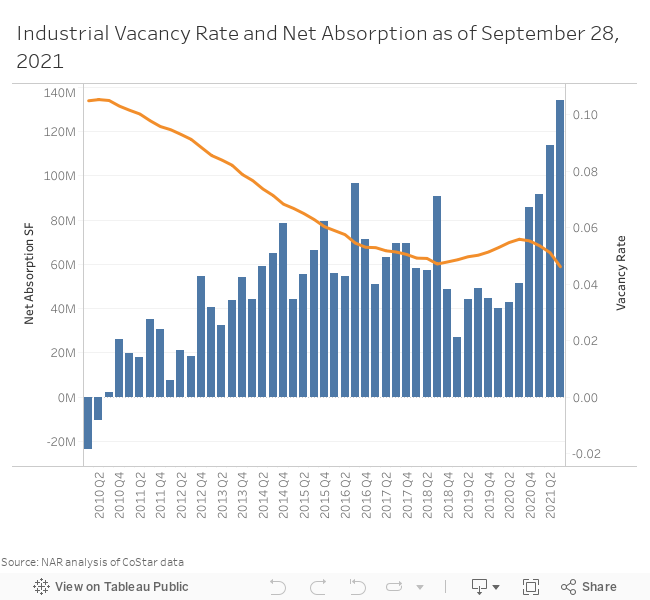

From 2020 Q2 through September 28, 2021, more than 518 million square feet of industrial space has been absorbed by the market (positive net absorption), according to CoStar® market data. Of the 518 million square feet, the majority, 94% or 486 million square feet, is comprised of logistic space. The industrial vacancy rate has decreased to 4.6% (5.3% in Q1 2020) as downward pressure is largely due to more demand for quality industrial space than supply can manage, which is a result of the acceleration of e-commerce.

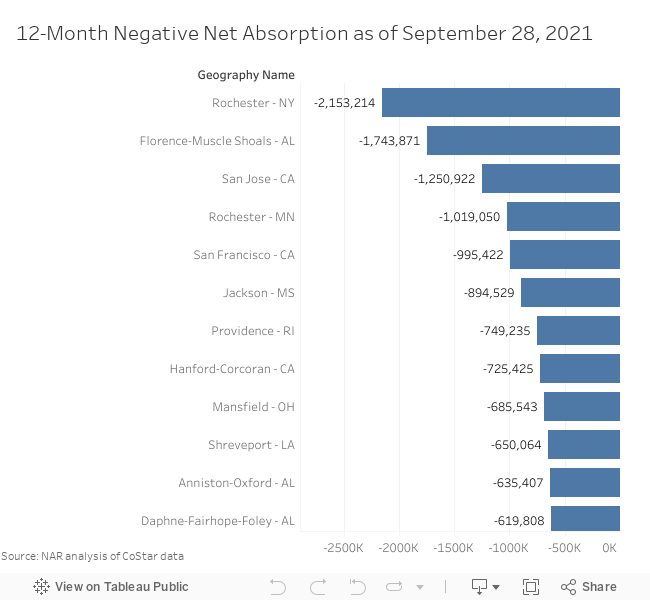

As of September 28, 2021, Rochester, NY; Florence-Muscle Shoals, AL; San Jose, CA; Rochester, MN; San Francisco, CA; Jackson, MS; Providence, RI; Hanford-Corcoran, CA; and Mansfield, OH have seen the largest declines in occupancy over a 12-month period. Of particular note, of the top 10 markets with the largest deficit in net absorption over the past 12-month period, 30% are in the West and in California in particular. According to CoStar® market data, 86 of the 390 markets covered have released industrial space back to the market (negative net absorption) and of those markets that have returned industrial space to the market, 4 have lost over 1 million square feet in industrial occupancy on a net basis over the past 12 months ending September 21.

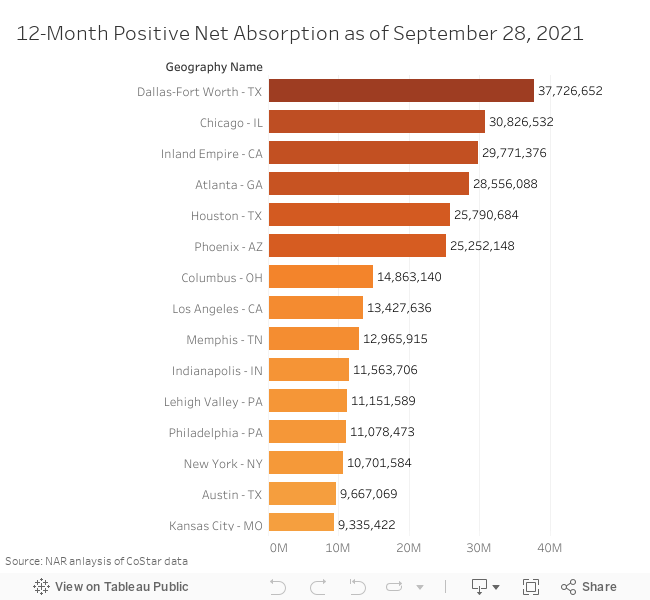

Both gateway cities and secondary markets are experiencing rising occupancy, with the largest increases occurring in Dallas-Forth Worth, TX; Chicago, IL; Inland Empire, CA; Atlanta, GA; Houston, TX; Phoenix, AZ; Columbus, OH; Los Angeles, CA; Memphis, TN; and Indianapolis, IN, each of which absorbed at least 10 million square feet of industrial space.

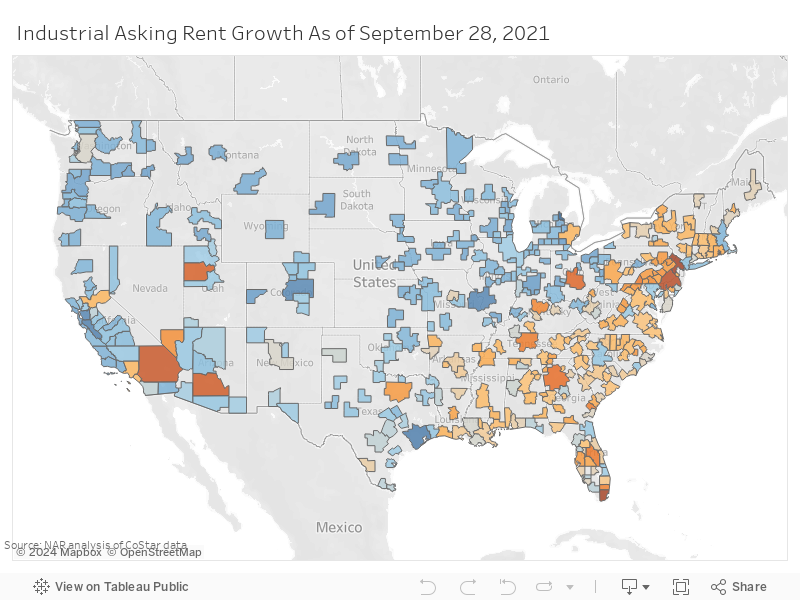

The continued tight market conditions and increased demand for industrial space brought with it an increase in rental growth as the year-over-year average asking rent has increased to 6.9%, which is up from 4.6% in Q2 2020 and Q1 2021 and 5.6% from Q2 2021. Logistics rents rose 7.9% as of September 28, up from 6.6% in Q2 2021 and up from 5.0% in Q2 2020. Flex space and specialized industrial space were up by 4.7% and 5.8% respectively.

According to CoStar® data, the industrial rents are up on a year-over-year basis across all 390 markets covered with the highest rent increases in Northern New Jersey (13.0%), Miami (12.7%), Philadelphia (12.0%), Inland Empire (11.4%), Phoenix (11.2%), Salt Lake City (10.9%), Columbus (10.7%), Atlanta (10.3%), Chambersburg-Waynesboro (9.8%), and Orlando (9.8%).

Solid demand for industrial space will continue. Net absorption for industrial space has already surpassed 339 million square feet in 2021 thus far, with expectations to finish the year on a high note. With new supply coming to market, the overall vacancy rate will face some upward pressure as quality space will provide more options for occupiers to consider, while asking rents will continue their upward trend as positive year-over-year growth continues for the remainder of 2021 and beyond.