After five consecutive years of solid gains, home price growth in 2018 is likely to calm down measurably and rise by only 2% on a nationwide basis.

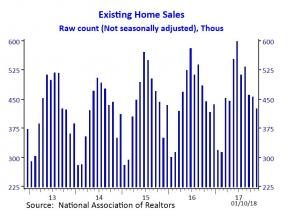

Existing-home sales rose 5.6 percent in November from one month prior while new home sales increased 17.5 percent.

The new tax law reduces the limit on deductible mortgage debt and limits the deductibility of the real estate tax up to $10,000.

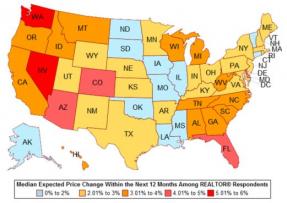

Among REALTOR® survey respondents, the median expected price change for the next 12 months was 2.9 percent.

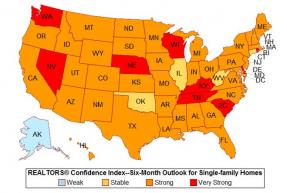

REALTORS® broadly expect sales to be “strong” than “weak” in the next six months across property types.

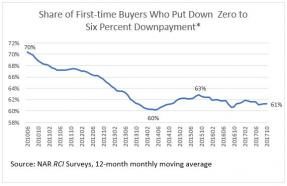

Why has the share of first-time buyers who obtained low downpayment mortgages not budged up significantly even with these low downpayment conventional financing programs?

Based on the new tax law, there is no change for capital gains on the sale of a home and deductibility of interest paid for a second home. However, the new law affects the deductibility of mortgage interest and real estate taxes.

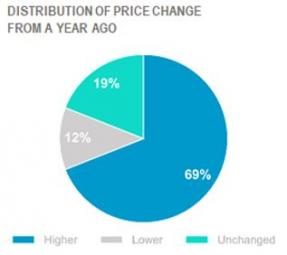

The national index level in October reached a new high and is up 6.2 percent from a year earlier.

In 2017, the time on market plummeted to an all-time low—at just three weeks—to sell a home.

REALTORS® report “low inventory” and “tax reform” as the major concerns affecting transactions in November 2017.

Search Economists' Outlook