Gen Xers, buyers aged 39 to 53 years, made up the second largest share of home buyers by generation at 24 percent of all home buyers in 2018, down from 26 percent last year.

Respondents to the February REALTORS® Confidence Index expect home prices to typically increase by 1.9 percent nationally, up from 1.4 percent in the January survey.

While most industries are experiencing a new high in total jobs in their sectors, the construction industry is still not back to its prior peak.

Older Millennials, buyers aged 29 to 38 years, made up the largest share of home buyers by generation at 26 percent of all home buyers in 2018.

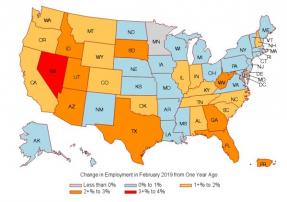

All states gained jobs, except for Minnesota and Rhode Island, with the strongest job growth occurring in the West region.

Younger Millennials, buyers aged 21 to 28 years, made up 11 percent of all home buyers in 2018, surpassing the Silent Generation as a buying group.

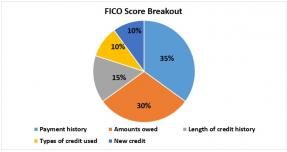

A credit score significantly determines the terms of your loans and whether you can afford these loans or not. Credit scores are used in evaluating a range of loans such as personal loans, car loans, and home mortgages, so credit scores are equally important for both renters and homeowners.

First-time buyers accounted for 32 percent of sales (29 percent in February 2018).

In the last six years home prices increased 47 percent while wages rose 16 percent. What do these percentage changes actually mean for a typical homebuyer? How much did the typical salary increase in dollars? How much more do buyers need to pay for their monthly payment because of the price increase?

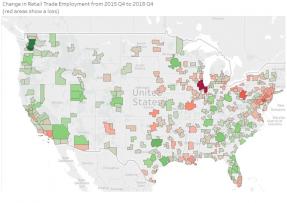

E-commerce continues to challenge brick-and-mortar retailers, especially department stores and sporting goods, hobby, book, and music stores. However, the retail trade sector is still facing bright prospects in growing metro areas that are attracting people, jobs, and housing.

Search Economists' Outlook