This blog post was written by George Ratiu, Director of Quantitative & Commercial Research and Erin Fitzpatrick, Research Intern....

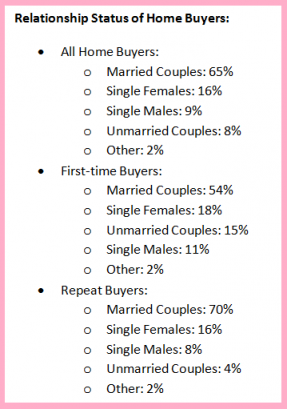

Using data from the 2014 Profile of Home Buyers and Sellers and 2013 Home Features Survey we can break down household composition, and the relationship it has to home purchasing choices.

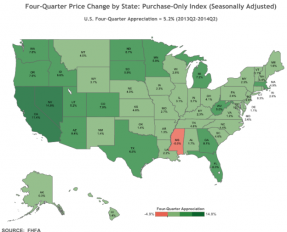

Earlier this week, we looked at the FHFA and Case-Shiller release focusing on national data trends. Today, we’ll dig a bit deeper to look at more local data at the regional, state, and city or MSA level.

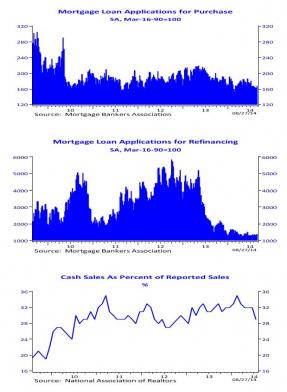

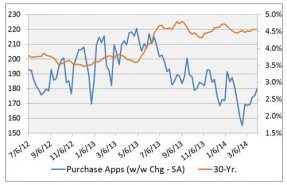

More people filed applications to take out a mortgage in the past week. Applications for buying a home rose 3 percent from the prior week. They are still down 11 percent from one year before....

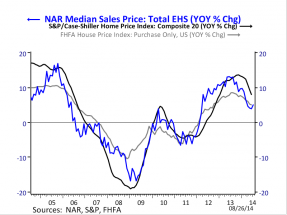

Last week NAR released median home price information that showed gains of 4.9 percent in July 2014 home prices compared to July 2013. This gain was slightly higher than the 3.7 percent seen in June and notably slower than double-digit price growth in summer/fall 2013.

Seasonally adjusted applications to purchase homes rose 2.7% for the week ending April 4th, the 4th consecutive increase. The purchase index is 13.9% lower than the same time in 2013. Purchase applications appear to have bottomed relative to last...

Seasonally adjusted applications to purchase homes ticked upward 0.9% for the week ending March 28th, the 3rd consecutive increase. The purchase index is 17.3% lower than the same time in 2013. Purchase applications appear to have hit or are...

To gain insight on the impact of the new law, NAR Research surveyed a sample of lenders with questions about the effect on their business and how the rule could in turn affect consumers.

Last week NAR released existing home sales and median home price information that showed gains of 9.1 percent in prices in February 2014 compared to February 2013, notably slower than trends in early summer/fall 2013 when price growth topped a double-digit pace.

The qualified mortgage (QM) rule was implemented in January of 2014. This law is intended to protect consumers by strengthening underwriting standards, but some have argued that the rules will raise costs and reduce access for consumers.

Search Economists' Outlook